What happened in the first quarter of 2026? What lies ahead in the coming months? How many YNG tokens were issued, bought and sold — and what are the next steps?

2026 began with the same spirit that closed the previous year: the drive to turn promises into action. If 2025 was the year we redefined our horizon, this first quarter saw that horizon become concrete. The standout event of these months was undoubtedly the rollout of the payment account and debit card.

Despite the milestones achieved, the context in which we have operated has been anything but simple. Early-year expectations pointed to a decisive recovery, but we have had to contend with a global market held back by a tense international climate. In this uncertain scenario, our ecosystem has demonstrated lower volatility compared to the main market assets in the reference period: the YNG token has withstood the impact with a stability that confirms how its value is now anchored to solid foundations and to the utility real within the app.

The payment account and the debit card represent only the first version of a much larger project. This foundation is the starting point for building the super app we have in mind, a vision that will take concrete shape in the coming months. In the meantime, we are working to expand the ecosystem through targeted marketing activities: capturing an ever-growing share of customers is vital for the token and for the ecosystem which, in our view, still presents wide margins for development and organic growth relative to the expressed value.

The climate for the coming months is one of great momentum. The MiCA authorisation deadline is approaching and our dossier is under review by the authorities, while prize competitions and engagement mechanics continue to evolve. We are also working on a new feature, previewed exclusively to Club members during the Winter Summit 2026, which adds a further element to our offering. Welcome to the report on the Young (YNG) token for the first quarter of 2026. Happy reading!

Price Analysis: YNG’s Resilience

To frame YNG’s performance this quarter, look at the market’s ‘king’: Bitcoin lost around 15% year-to-date, with a drawdown exceeding 30% at its worst point in February. Against this backdrop, YNG moved in the opposite direction, limiting losses to 5%. Despite being roughly halfway from the October 2025 all-time high, volatility was well below the sector average.

Key technical levels:

- Resistance: the barrier to break sits at €0.49, the peak reached after the Uniswap listing.

- Support: the €0.41 zone proved a solid floor, holding throughout the quarter.

How long this consolidation phase lasts will depend largely on easing international tensions. A de-escalation could restore confidence in risk assets and Bitcoin, reigniting retail investor enthusiasm that has been absent for some time. We will not simply wait. We continue working to be ready when the wind changes. Details on new listing plans and our expansion strategy are reserved for Club members.

Payment Account and Young Card

The launch of the Young payment account and debit card is the first concrete step toward the super app we want to build — a financial ecosystem that brings together everything a user needs, from daily cash management to the crypto world, all under one roof.

At the heart of this vision is a simple idea: there is no app today that addresses two deep needs of the Italian saver. The first is the safe custody of personal finances, with immediate access to the sector’s most advanced tools. The second is financial education — ongoing guidance that asks the right questions about spending habits and encourages saving and investing in a conscious, safe way. This direction was central to the workshop presented at the Starting Finance Investment Meeting, where the team shared Young Platform’s vision as an active financial education tool.

The technical core of this first version is the Italian IBAN assigned to every user. The strategic advantage lies in the integration with the exchange: transferring funds between the account and the crypto wallet is instant and commission-free.

The physical debit card introduces a new dimension for the YNG token. Every purchase generates a YNG cashback, transforming the token from a simple digital asset into a strategic resource that can be accumulated every day. The tokens earned are not just a reward — they are the key to levelling up in the Clubs.

To accelerate adoption, we activated a dedicated promotion: the first 1,000 users who sign up in April will receive a 3% cashback for 90 days, regardless of their Club tier.

From Layer 0 to Future Evolutions

What we released is what we call the “Layer 0“: a solid foundation to build on. The roadmap is already defined:

- Integration of the digital card with Apple Pay and Google Pay

- Analytics tools for conscious spending monitoring

- A dedicated Save section for savings

The goal is not marketing for its own sake, but building a financial model that genuinely simplifies users’ lives by bringing accounts and exchanges together. Each new feature will be another step toward an app that does not yet exist in the market.

Tax Services: Zero Stress, Full Clarity

It’s that time of year nobody particularly enjoys, but which must be tackled with the right tools: the tax return. Italian crypto tax regulation has become a maze, which is why for three years we have been turning what was a simple Excel file into a complete ecosystem of tax solutions. Our tools are ready to cover every need for the 2025 tax year.

Young Platform Tax Report

For users of our exchange only:

- Standard user: from €19.99 (under 50 transactions) to €49.99 (over 500 transactions)

- Club Essential: from €15.99 to €39.99

- Club Silver: from €13.99 to €34.99

- Club Gold: from €11.99 to €29.99

- Club Platinum: from €3.99 to €9.99

Young-Okipo Tax Report

For users active on DeFi, NFTs and other exchanges:

- Standard user: €79

- Club Essential: €69

- Club Silver: €59

- Club Gold: €49

- Club Platinum: €44

The New Rules: 26% or 33%?

The 2026 Budget Law introduced a key distinction:

- 33% rate: for exchanging crypto for euros, dollars or dollar-pegged stablecoins (USDT, USDC).

- 26% rate: for euro-pegged stablecoins (such as EURC).

Crypto-to-crypto swaps (e.g. BTC to ETH) remain tax-neutral. However, with the abolition of the €2,000 allowance, every euro of capital gain must now be declared.

Using YNG tokens to activate a Club not only brings cashback on the card — it also cuts the real costs of tax management. Proof that the token is not just an asset to watch on a chart, but a tool that saves real money every time you deal with bureaucracy.

Real-World Presence

As previewed in the Q4 2025 report, 2026 was set to mark a decisive shift in our physical presence. We delivered on that commitment, building a plan for ongoing community engagement through direct interaction and institutional participation. What you are reading is only the first chapter in a series of events we will continue to promote.

Young Platform Winter Summit: The Way to the Top

On 8 March 2026, the Platinum Experience launched with the “The Way to the Top” summit at Skyway Monte Bianco. The event, reserved for partners and the most committed Club members, took place at 3,466 metres above sea level — an exceptional setting to preview the YNG ecosystem roadmap in an authentic networking environment.

The energy and feedback from participants confirm that direct closeness between the team and the community is essential for building something that lasts.

Starting Finance Investment Meeting

Young Platform participated as Gold Sponsor at the Starting Finance Investment Meeting 2026 in Rome, one of Italy’s leading events dedicated to financial education and markets. Two key moments:

- The team presented Young Platform’s development strategy toward the super app model and the vision for active financial education.

- A workshop explored the cognitive biases that influence investment decisions, focusing on practical tools to recognise and reduce their impact.

The success of the 5% cashback promotion at our stand demonstrated strong interest in the new integrated features. These events are the starting point of a journey to make Club membership a tangible advantage.

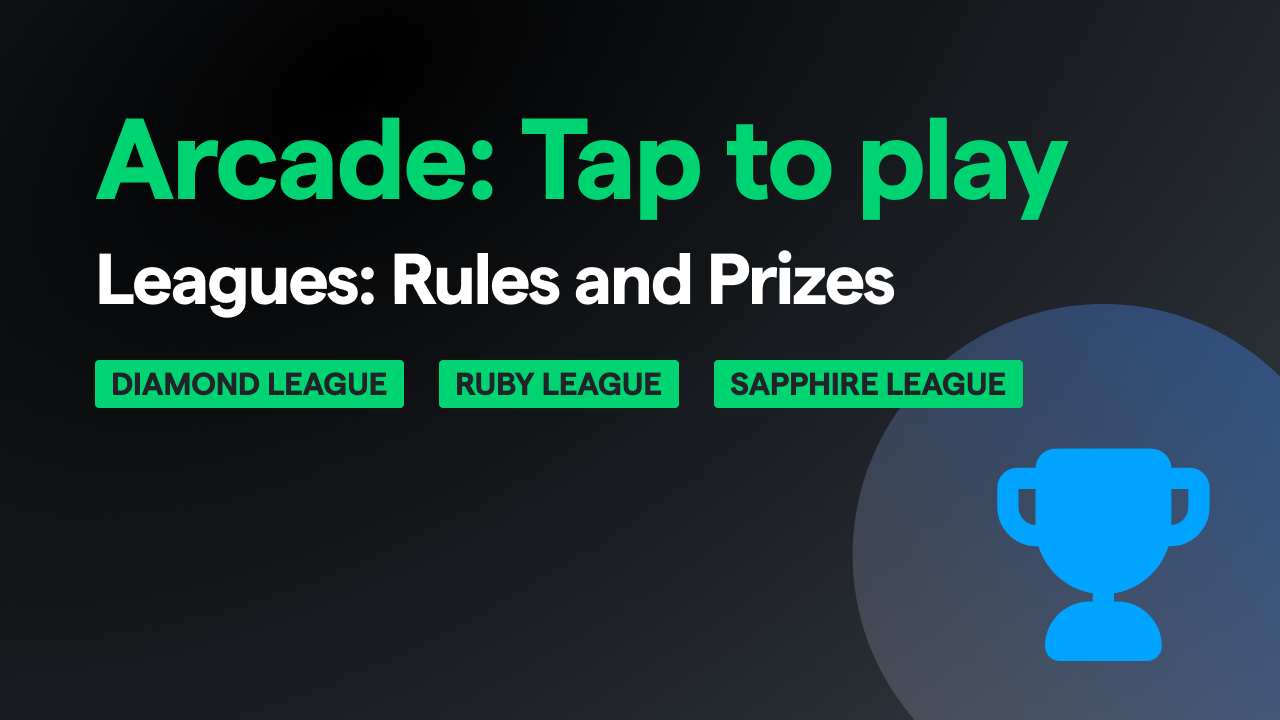

Arcade: Tap to Play

On 10 March, the Young Platform contest trilogy concluded with the end of The Reveal. After the success of The Box and The Unbox, this final phase marked the community’s engagement peak, with iconic prizes such as Rolex watches and KTM motorcycles.

With the trilogy complete, we launched Arcade: the new permanent gamification hub. Arcade is not just a prize draw — it’s a section of the app designed to turn every saving and investment choice into concrete rewards. The philosophy remains to incentivise virtuous financial behaviour through fun and consistent participation.

The key innovation is the Tap to Play mechanic:

- Daily interaction: users are encouraged to open the app and engage with the ecosystem, keeping attention on their assets and the platform’s latest features.

- Democratised rewards: following the tier system already tested successfully, Arcade lets anyone be competitive — what matters is consistency, not just financial capacity.

- Future vision: Arcade is the tool we are using to dismantle the boredom of traditional finance, one tap at a time.

With Arcade and Tap to Play, managing your financial health stops being a passive obligation and becomes an active, rewarding experience.

Exclusive Content for Club Members

As always, the most strategic analyses and sensitive data are reserved for Club members. In the Club-exclusive version of this report you will find:

- Updates on the Young Platform payment account and debit card

- Exclusive Club data: updated membership figures and analysis of the impact of member purchases on token performance

- Future roadmap: strategies and plans for upcoming listings on other centralised exchanges

Your support as Club members remains our most valuable resource.

Promotional content: the information contained in this report is for purely informational and educational purposes. Data regarding distribution, treasury reserves, and liquidity reflect the situation recorded in the first quarter of 2026 and do not constitute a guarantee of future price stability or the value of the YNG token. Access to DeFi protocols via third parties involves risks inherent to smart contracts and the volatility of crypto-assets. Buybacks and liquidity activities are carried out at the Company’s discretion and do not obligate the latter to any future market support interventions. We recommend consulting the Terms and Conditions and acting with awareness (DYOR). Young Platform does not provide financial advice.