On Young Platform you can deposit instantly with BANCOMAT Pay: add funds to your account simply, securely and immediately — with no need for bank transfers or cards.

Spotted a market opportunity but haven’t got the funds available in your wallet to act right away? Now you can fix that in a matter of seconds. No codes to enter, no waiting: a few taps are all it takes to complete the transaction and get back to business.

How to use it

Making a deposit with BANCOMAT Pay is simple:

Go to the Deposits section in the Young Platform app.

Select BANCOMAT Pay as your method.

Enter the amount you wish to deposit.

You’ll receive a notification from the BANCOMAT app or from your bank’s own app, if it offers the service.

Authorise the transaction directly from your device.

The funds will be available in your wallet straight away.

The transfer runs on the BANCOMAT network and uses SEPA Instant technology, ensuring maximum speed and security.

The benefits of BANCOMAT Pay

BANCOMAT Pay is designed to offer a smooth, efficient deposit experience. It lets you top up in real time, removing the waiting times that come with traditional banking systems. It doesn’t require you to enter sensitive data such as your IBAN, thanks to a fast authentication system that complies with banking security standards (SCA – PSD2).

But BANCOMAT Pay isn’t limited to deposits: it’s a complete digital payments ecosystem. You can use it to shop in store or online, and to send and receive money using a mobile number, without having to share your banking details. It’s ideal for small everyday expenses, such as splitting the bill at a restaurant or paying a friend back.

Its simple, intuitive interface makes it accessible even if you have little experience with payment apps.

Who can use BANCOMAT Pay

To use it on Young Platform, you need:

a current account or a card with a bank that participates in the network;

a mobile number linked to BANCOMAT Pay or to the integrated banking app.

The service does not work with foreign accounts that are not compatible with the Italian network. If you live abroad or use an unsupported account, you can always top up your wallet by SEPA transfer or card.

Fees

From 4 September 2026, BANCOMAT Pay deposits are subject to the following cost structure:

Percentage fee:2.2% of the amount deposited.

Minimum fee:€0.25 per transaction.

For more details, and to check the most up-to-date conditions at any time, see the “Fees and pricing” section of the Young Platform app

Operating limits

Young Platform applies the following limits to BANCOMAT Pay deposits:

Daily limit: €1,500

Weekly limit: €3,000

Monthly limit: €30,000

The limits are cumulative and refer to the total amount deposited, regardless of how many transactions you make.

How to activate BANCOMAT Pay

BANCOMAT Pay is available inside the BANCOMAT app. Some banks integrate BANCOMAT Pay natively into their own app. In those cases, there’s no need to download the BANCOMAT app separately, because the service is already available. Find the banks that participate in the service at this link.

If your bank doesn’t integrate BANCOMAT Pay, you’ll need to set up the official app.

Activation procedure:

Download the BANCOMAT app from your app store.

Enter the mobile number linked to the account you intend to use.

Follow the authentication procedure indicated and required by your bank (activation code, QR code).

Link your current account to BANCOMAT Pay.

Enable a secure recognition method (fingerprint, face or PIN).

Once activation is complete, you’ll be able to use BANCOMAT Pay to deposit funds on Young Platform, pay in shops and send money in real time.

Why choose BANCOMAT Pay

BANCOMAT Pay is a service from BANCOMAT S.p.A., the company that runs Italy’s main electronic payment network. Founded in 1983, it is today a byword for innovation, security and reliability.

Millions of Italians use BANCOMAT every day to pay and withdraw cash.

BANCOMAT Pay is integrated into the leading Italian banking apps and allows payments by mobile phone without sharing your IBAN. It’s built to be fast, secure and suited to everyday use.

What’s more, thanks to the European EuroPA project, it is compatible with digital wallets in other countries, such as Bizum (Spain) and MB WAY (Portugal), making the service even more complete and interconnected across Europe.

Help and support

If you run into problems installing or using BANCOMAT Pay, you can:

With BANCOMAT Pay on Young Platform, topping up your wallet is faster, more practical and more secure. A few taps and you’re ready to seize the next market opportunity.

A personal Account Manager, all to yourself: the new benefit of the Gold and Platinum Clubs

There comes a moment, for anyone operating in crypto, when the FAQs are no longer enough. You have an important transfer to make and want to be sure of every step. You want to understand how a service works before activating it. You have a specific operational question and would simply like to talk it through with a person — the same person, every time, who knows you and your history on the platform.

From today, that person exists: they are called your personal Account Manager, and they are the new benefit reserved for members of the Gold and Platinum Clubs.

A person, not a ticket

Your Account Manager is your dedicated point of reference within Young Platform. Not a different operator with every request, not a support queue: a professional with a name and a surname, who gets to know the way you use the platform and follows you over time.

Here is what they can do for you:

Priority, dedicated assistance: your requests travel in a fast lane, with response times reserved for Gold and Platinum members.

Step-by-step operational support: deposits and withdrawals of significant amounts, transfers from other platforms or wallets, checking the correct networks, OTC transactions — your Account Manager accompanies you through every stage, so that everything is carried out safely.

Guidance across products and services: from the Tax Report to the Account and Young Card, from live promos to what’s coming next, they explain how each service works, what it includes and how to activate it.

What it is not (and it’s right that you know)

Transparency first: your Account Manager does not provide investment advice, nor tax or legal advice. They will not tell you which crypto-assets to buy or sell, will not make personalised recommendations and will not assess your portfolio: every investment decision remains exclusively yours. Their role is to make your life simpler on the operational and informational side.

Book your video call directly from the app

The beauty of this benefit is also how simple it is to use. No emails, no waiting: the video call with your Account Manager can be booked in a few taps, directly from the app.

Open the Young Platform app and go to Profile.

Enter the Club section.

Tap the Account Manager benefit and choose a date and time from the available slots: your video call is booked.

You can book whenever you like, reschedule if something comes up and find every appointment in your calendar. Your Account Manager joins the call already briefed on your request.

Note –This benefit has been added in the latest Young Platform app update: download it now so you don’t miss out on what’s new!

Who it is reserved for

The personal Account Manager benefit is included in the Gold and Platinum Clubs, at no additional cost beyond your Club level. If you are currently Silver or have not yet joined a Club, you can find the requirements, benefits and conditions of each level on the dedicated Club page and in the related Terms and Conditions.

This is a marketing communication within the meaning of Regulation (EU) 2023/1114 (MiCA). The “personal Account Manager” benefit is a dedicated assistance service reserved for members of Young Platform’s Gold and Platinum Clubs, subject to the Club Terms and Conditions available at youngplatform.com/legal. The Account Manager provides exclusively operational and informational support on Young Platform’s products and services and does not provide investment, tax or legal advice, nor personalised recommendations on crypto-assets; every investment decision is taken independently by the user. Crypto-assets are highly volatile and carry a significant risk of loss, including the total loss of the capital invested; they are not covered by bank deposit guarantee schemes (Directive 2014/49/EU) or investor compensation schemes (Directive 97/9/EC). Young Platform reserves the right to modify Club benefits for the future, as provided for in the related Terms and Conditions. Crypto-asset services are provided by Young Platform S.p.A., Via F. Cigna 96/17, 10155 Turin, Italy — VAT no. 11931440017 — authorised by Consob and the Bank of Italy to operate as a Crypto-Asset Service Provider (CASP) under Regulation (EU) 2023/1114 (MiCA). Contractual and economic conditions in the Information Sheets and Terms & Conditions at youngplatform.com/legal.

The second quarter 2026 report on the YNG token. What happened, and what changes with the MiCAR licence?

What happened in the second quarter of 2026? How did the YNG token move in a period that was anything but easy for the market? How many tokens were issued, repurchased and distributed, and what changed with the MiCAR authorisation?

Young Platform’s second quarter of 2026

One date marks this quarter more than any other: 30 June. On that day Consob and Banca d’Italia authorised us to operate as a CASP, that is, as a crypto-asset service provider under the European MiCAR regulation. It arrived on the very last day available, when the transitional regime that had accompanied the sector until then expired. From that point on, in the European Union, only those who are fully compliant can operate.

And there is a change that concerns this very report. For several quarters, part of its content was reserved for Club members: a little extra depth for those closest to the project. From today that is no longer the case, and the reason is, once again, MiCAR: information that can affect the YNG token must be accessible to everyone at the same time and on the same conditions, with no privileged channels. So the report goes back to being what it once was, public and open to anyone, from the first figure to the last.

The market context we moved in, however, was anything but favourable. After a recovering April, the market slowed in May and fell back decisively in June, closing the quarter clearly down. Against this backdrop the YNG token showed, over the period, lower volatility than the sector’s leading assets: in the toughest month, June, it limited its losses to a fraction of those recorded by Bitcoin and Ethereum. This figure refers to a single quarter and to a limited number of comparison assets: it does not imply that YNG is, in general, a less risky investment, nor does it constitute a recommendation to buy, sell or hold the token.

The authorisation, though, is not a finish line: it is the ground our work will stand on from here on. And the weeks immediately after the close of the quarter have already shown it: we launched a campaign dedicated to those who bring their assets onto the platform, we introduced YNG Boost, our vesting service that rewards with additional tokens anyone who buys YNG and locks them on the platform for a period of their choosing, another route, alongside the Clubs, to give the token a concrete role, and, above all, we are bringing the YNG token onto a new international trading venue.

What will you find in this report? The lead role, as the title says, goes to the Young (YNG) token: how the price moved, how many tokens were issued and repurchased, how the circulating supply was distributed. But also everything that, around the token, accompanied its quarter: from the card cashback to the buyback programme, from the Clubs to the developments of the past few weeks. The complete data, with all the on-chain addresses and regulatory references, remain in the official informational communication, which we are publishing alongside this report.

Welcome to the Young (YNG) token report for the second quarter of 2026. Enjoy the read!

The MiCAR licence, and what really changes

Let’s start here, because it is the chapter that weighs most of all. The authorisation covers 8 of the 10 services set out in the regulation: from the exchange of crypto-assets to custody, from advice to portfolio management. In practice, almost everything we offer every day in the app is governed by a European regulatory framework.

What does it mean, in practice, for those who use Young Platform? The truth is that, in everyday use, little or nothing changes: the app is the same as ever. What changes is the picture around it, both for the market and, potentially, for the path ahead of us. The most immediate consequence is this: with the expiry of the transitional regime, operators without authorisation had to leave the European market. Those who remain are the ones that completed the process required by the authorities, a detail that is anything but secondary, in a sector where for years the word “rules” was more the exception than the norm.

Then there is an effect set to count above all in the months to come: thanks to the European passport, the licence obtained in Italy allows Young Platform to operate across the entire Union: no new authorisation is needed in each member state, only a notification to the competent Authority of the host country. To date the notification relating to France has been completed.

The price of YNG and the state of the market

Let’s get to the price, usually the first item you go looking for. Over the quarter, the YNG token went from €0.4428 on 31 March to €0.574 on 30 June: +29.6%.

A number on its own, though, tells only half the story. The context in which that number matured was anything but simple. After a recovering April, with the total crypto market capitalisation up around 13%, May slowed and June braked hard: around -20% in a single month, down to about $2.02 trillion, the lowest level in almost two years. Bitcoin closed June at -21.6%, Ethereum at -23.9%.

In that difficult month YNG moved between €0.529 and €0.572, closing at -8.4%. A decline, certainly, but a more contained one than that recorded by the sector’s big names over the same period.

Account and card: the effect on the token

The Young payment account and debit card are not new to this quarter, we covered them at length at their debut. They had been introduced earlier, with a gradual rollout initially reserved for Club members; it was on 20 April that access opened to the entire user base. They come back into the report because it is in these months that they began to leave their mark on the token.

The first channel is cashback: every purchase with the card gives part of it back in YNG tokens, with a percentage that rises with the Club level, from 0.1% for Essential up to 3.60% for Platinum. The more the cards are used, the more YNG enter users’ wallets. This does not mean, however, that the tokens in circulation have exploded: as we will see further on, issuance has stayed under control. It is a principle we have always cared about, ever since we revised the way YNG is issued with the 2023 Step update.

The second channel is less visible, but for the token it counts a great deal. On every transaction with the card there is a small 0.15% fee that flows directly into the buyback programme: every payment with the Young card becomes, in a fraction of itself, fuel for repurchasing YNG on the market. It is the fourth source feeding the programme, alongside staking fees, those from the decentralised pools and those from Young Platform Step.

Buyback and liquidity additions

And since we have just mentioned it: what exactly is the buyback? We have talked about it in several reports, but it is worth restating; not least because, as we were saying a moment ago, the card has just become a new source feeding it.

It is the mechanism by which part of the ecosystem’s revenues comes back to the token. It works in monthly cycles, and it is easier to understand with an example.

Imagine that, in a given month, the ecosystem generates a certain sum earmarked for the programme. The following month those funds are put to work in two moves, in this order.

First, the liquidity of the YNG/USDC pool on Uniswap is strengthened: more liquidity means smoother trading and prices less prone to sharp swings.

Then, if anything is left over after that operation, the remainder is used to buy back YNG directly on the market.

And the repurchased tokens? They don’t disappear: they stay in the treasury and the following month become the first brick of the new liquidity injection. A cycle that feeds itself, month after month.

Two things we make a point of repeating in every report, because they head off misunderstandings. The first: the repurchased tokens are not burned, but stay in the treasury. The second: the buyback is not an operation to support the price. It promises no levels, it is not a commitment to intervene in the future. It is, much more simply, a transparent way to recirculate revenues within the ecosystem. The programme is run at Young Platform’s discretion and may be amended or discontinued at any time.

Here is what was actually done during the quarter:

April 2026 (€2,591): repurchase of YNG on the market and rebalancing of the pool.

May 2026 (€2,802): to which are added 695 USDC and 773 YNG of fees accrued from the pools, reinvested in the YNG/USDC pool.

June 2026 (€4,368): the month’s revenues were used entirely to buy USDC, funding the liquidity addition of the 10,188 YNG left in the treasury from previous months.

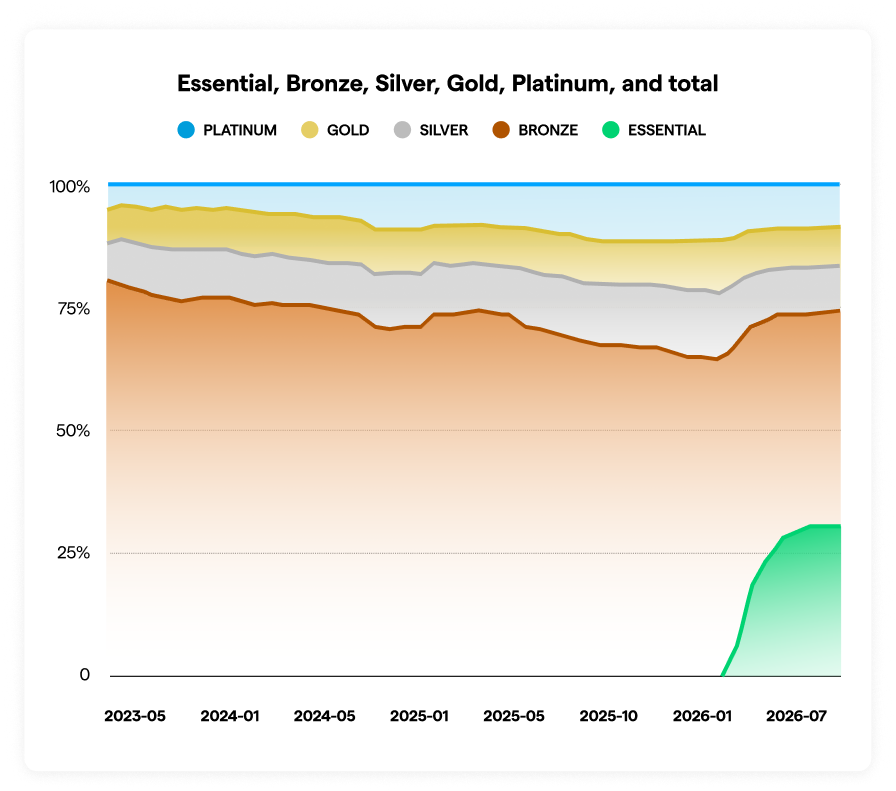

The Club numbers

YNG is Young Platform’s utility token and gives access to the Clubs: the subscription plans that offer benefits on our crypto services and on a selection of brands designed for everyday life. As at the 22 July measurement there are 2,440 Club members, broken down as follows (in brackets, the change from the previous report):

Bronze: 997 (-2.9%).

Essential: 801 (+9.4%).

Silver: 254 (-4.5%).

Gold: 202 (+11.0%).

Platinum: 186 (-1.1%).

Overall the number of members grew by 1.9%. The drivers are the Gold (+11%) and Essential (+9.4%) levels, while the others remain substantially stable.

The number of members is not an incidental figure: it is directly linked to the distribution of the token. The more people join a Club, the greater the quantity of YNG voluntarily locked on the platform, and therefore the smaller the circulating availability.

Distribution of the YNG token

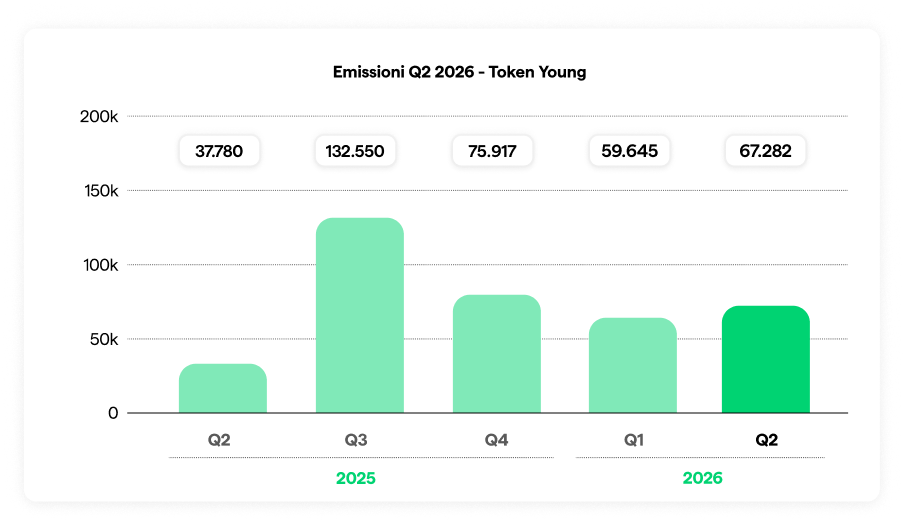

At the end of March the circulating supply was around 27.66 million YNG; at the end of June, with the quarter’s issuance, it rises to around 27.73 million. A net increase of just over 67,000tokens, equal to around 0.24%: issuance remains contained, as the model provides for.

These new tokens were distributed through several mechanisms:

30,153 YNG through Step;

33,839 YNG through the card cashback;

3,290 YNG through staking.

That cashback is already the largest item, just two months after the card opened to all users, shows how quickly this channel is taking hold. The maximum quantity of YNG nevertheless remains fixed at 100 million, with no mechanism that generates new ones beyond that threshold or destroys them.

On the liquidity front, YNG can be traded on two decentralised pools on Uniswap. At the close of the quarter they contained:

YNG/USDC pool: around 1,376,889 YNG and 897,951 USDC;

YNG/WETH pool: around 345,096 YNG and 117.4 WETH.

Compared with the end of March, the YNG share fell in both pools, while that of the paired asset (USDC and ETH) grew: the effect of the buyback programme’s rebalancing interventions, which strengthen market depth.

The quarter’s activities

The quarter closed on 30 June, but the pace did not slow: several initiatives started right at the turn between the end of the period and the weeks that followed. We gather them here.

The launch of YNG Boost

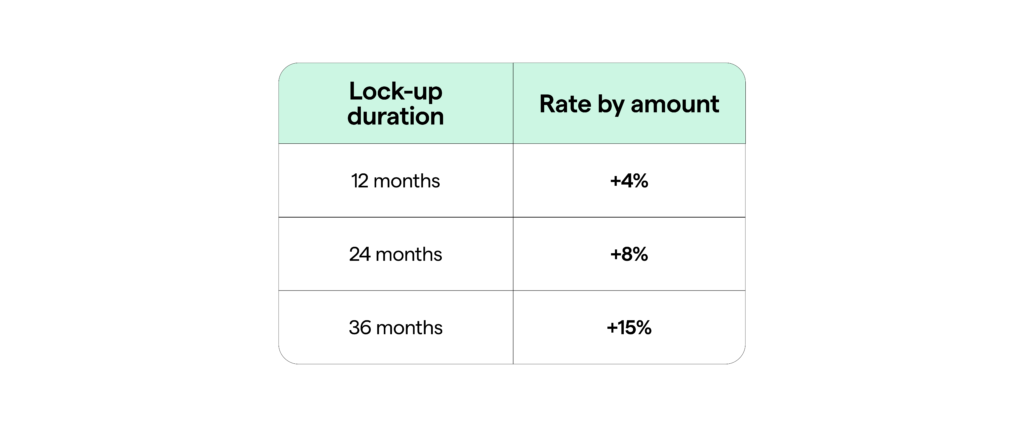

With YNG Boost (the Vesting Service) we have opened a new route for those who want to back the token over time. How it works is straightforward: you buy YNG at market price, you agree to lock them on the platform for a period of your choosing (12, 24 or 36 months) and, in exchange, you receive an additional quantity of tokens. It is not a yield or an interest payment: it is a quantity of YNG that we disburse from our treasury, in our capacity as issuer, to support those who choose to stay and look to the long term.

The Boost grows with the amount and the length of the lock-up, and for Club members (Silver, Gold, Platinum) an uplift applies: it goes up to 34.5% in additional tokens.

Two clarifications we want to make: the Boost applies only to new purchases, selling and rebuying the YNG you already hold does not entitle you to the bonus, a rule designed precisely to protect the token’s market; and the percentages indicate quantities of tokens, not a yield: their value in euros can vary over time with market volatility. All the details are in the dedicated article as well as in the Pre-contractual Information for the Vesting Service.

Deposit campaign (MYCA) and the BNB listing

From 1 July to 2 August, Move Your Crypto Assets (MYCA) is running, the promo designed for those who want to move their crypto to Young Platform. It comes straight out of the MiCAR licence: now that the sector has clear rules and boundaries, bringing your funds back to an Italian platform, headquartered in Turin and fully regulated, is a choice in favour of transparency.

The mechanism is simple: a deposit of at least €1,000 is enough (in crypto, in euros or in a combination of the two) and the more you deposit, the higher the level you reach. The promo is split into three Tiers (from €1,000, from €10,000, from €50,000 upwards) and unlocks benefits on five fronts: a Bonus Wallet, the free Tax Report, an enhanced YNG cashback of up to 3.6%, dedicated conditions on the card and the account and, for the highest amounts, a personal Account Manager.

All the conditions are set out in the rules published on the website. Along the same lines, another development: since 16 July we have added BNB to the crypto available in the app. It is one of the most traded assets in the world, and the decision to list it now answers a precise need: to offer those who hold it a regulated and compliant place, in Italy, where they can carry on operating while the European regulatory framework redraws where and how certain assets can be offered.

The WhiteBIT listing

From 28 July, YNG will also be tradable on WhiteBIT, on the YNG/USDC pair. It is the token’s first listing on a third-party centralised exchange: until today YNG was accessible only on Young Platform and, since July 2025, on the decentralised protocol Uniswap as well. And WhiteBIT is not just any venue: it is a European platform that states it operates with a MiCAR licence in Austria and VASP authorisations in ten EU countries, over 8 million registered users and a daily trading volume of between $1 and $2.5 billion, the leading European exchange by web traffic, with around 32 million visits a month.

For the token, entering a venue of this size means three concrete things: more geographic visibility (WhiteBIT has strong roots in Eastern Europe, an area where Young Platform is still little present), an international proving ground in front of a community with different habits from ours, and one more point of access, alongside Young Platform and Uniswap.

The listing fits into a year that has changed the scale we operate on, the MiCAR licence and the €22.5 million capital increase led by Gruppo Azimut, and it will not be the last stop: the search for new trading venues for YNG will continue through 2026. One clarification, as always: a listing is a matter of infrastructure, not a promise about the price, and it affects neither the tokenomics nor the holders’ rights defined by the White Paper. We covered it all in detail in a dedicated article.

The DeFi Wallet

Among the developments we are working on, the DeFi Wallet is the one we look forward to most, because it changes what can be done on Young Platform. Until today, to put your crypto to work in decentralised finance you had to leave the app: open an external wallet, learn to manage it, move between several different tools and hope not to get a step wrong. With the DeFi Wallet all of this happens in a single place (inside the app you already use) and in a couple of taps.

It is a wallet whose control is entirely yours: the keys stay with you, we provide the interface to use them without complications. From there you will be able to put your crypto-assets to work on the sector’s most established lending protocols, on which much of DeFi is based, without having to become an expert in anything. And we are not flinging open a door onto the whole blockchain: access is limited to a selection of protocols we have vetted and judged solid. It is our way of bringing you the freedom of decentralised finance without the wild west that too often comes with it.

It will arrive the way all our things arrive: a bit at a time, first to groups of users and then to everyone. We are not giving a precise date (for the reason we explain below), but there is one thing we will say straight away, because it is right to know it: since it is a wallet you manage on your own, the DeFi Wallet falls outside the MiCAR scope and the regulation’s protections do not apply to what you do with your keys.

Conclusions

Those who have followed us for a while were used to a section on “what’s next” at the end of the report: a taste of what was cooking. From this quarter that section is gone, and it is worth explaining why.

With the MiCA authorisation, the YNG token and its issuer are subject to the regulation’s market abuse rules, including those relating to inside information. Information is “inside information” when it is precise, not yet public and, if disclosed, would be likely to have a significant effect on the price of the token. Previewing developments of this kind would mean giving readers an informational advantage over the market: exactly what these rules exist to prevent.

That is why the flow has changed. When information that can affect the price of YNG becomes communicable, the first step is no longer a post or a teaser: it is publication in the dedicated section of the website, where we collect the informational communications and, where the relevant conditions are met, the inside information relating to the token. That way everyone reads it at the same time, on the same terms. Our team, for its part, operates under the supervision of the authorities and with internal controls designed precisely to prevent anyone holding such information from taking advantage of it.

The upshot is that previews, as you knew them, will no longer be there. We realise it takes some of the flavour out of the wait. But it is, first of all, a protection for you: the guarantee that nobody, ourselves included, plays with information the market does not have yet.

This article is an overview, designed to give you the picture without drowning you in figures. If instead you want the complete data, with all the on-chain addresses and regulatory references, you will find them in the official informational communication, which we are publishing alongside this report.

This content is a marketing communication. The YNG token prices reported in this article are expressed in euros, the currency of the YNG/EUR market on Young Platform, where most trading is concentrated. Market data relating to Bitcoin, Ethereum and the overall capitalisation of the sector are expressed in dollars, in line with the convention of market sources. On-chain data is publicly verifiable via block explorer.

Past performance does not constitute a guarantee of future results, nor financial advice. The buyback programme is run at the discretion of Young Platform S.p.A., does not constitute a price support operation and does not guarantee any return. Access to decentralised protocols through the DeFi Wallet is a service outside the MiCAR scope and does not benefit from the protections provided for by Regulation (EU) 2023/1114. A White Paper compliant with Regulation (EU) 2023/1114 has been published for the YNG token, available on youngplatform.com: in the event of any discrepancy between this article and the White Paper, the White Paper prevails.

From July 28, YNG will also be tradable on WhiteBIT. A step that fits into a year of expansion for Young Platform: the MiCAR licence, the capital increase, and now a new international listing.

From July 28, 2026, the YNG token will also be tradable on WhiteBIT, a European centralised platform with a MiCA licence in Austria and VASP authorisations in ten EU countries. This is the first listing of YNG on a third-party centralised platform: until now, the YNG token was only accessible on Young Platform and, since July 2025, also through the decentralised protocol Uniswap.

What are the implications, and why now? To understand that, it helps to look at the year Young Platform has just been through.

A year of foundations

In 2026, Young Platform went through two milestones that changed the scale at which the company operates. The first is the MiCA licence: granted by Consob and the Bank of Italy, which authorised Young Platform as a CASP (Crypto-Asset Service Provider) for eight of the ten services provided for under the European regulation.

An authorisation that, thanks to the European passporting regime, is valid not only in Italy but, potentially, across the entire Union; the licence has now officially been passported to France as well.

The second is Young Group’s €22.5 million capital increase, led by the Azimut Group. Fresh resources to accelerate the build-out of a financial infrastructure that integrates crypto, digital banking and tokenised assets.

Taken together, the licence and the capital are the two conditions that make an expansion beyond Italy’s borders possible. And within that expansion, the YNG token, which sits at the centre of the Young Platform ecosystem, is one of the tools through which this path takes shape: the more accessible the token is across markets and platforms, the wider the audience that can come into contact with the ecosystem it represents. The listing on WhiteBIT is the first concrete step in this path.

Why WhiteBIT

WhiteBIT is a European exchange with a MiCA licence in Austria and VASP authorisations in ten EU countries, with over eight million registered users and a daily trading volume of between $1 and $2.5 billion, depending on the source. It is also the leading European exchange by web traffic, with around 32 million monthly visits.

For YNG, joining a venue of this size means three concrete things:

Greater geographic visibility: WhiteBIT was founded in Ukraine and has built a strong historical presence in Eastern Europe over time, a region where Young Platform is practically unknown. It’s an entry into a context the ecosystem currently has little presence in.

An international proving ground: the token is put to the test by a community with different habits and reference points from Young Platform’s historical one — a first concrete test of interest beyond its established audience.

More trading venues: YNG adds to the platforms already active — Young Platform and Uniswap — expanding the access points for anyone who wants to trade the token, regardless of channel or reference market.

A move that also reflects a broader choice of collaboration between platforms. “WhiteBIT is a natural partner in this phase of expansion, one that will let us bring YNG in front of an international audience“, commented Alexandru Stefan Gheban, CEO of Young Platform.

What doesn’t change

The listing has no bearing on the token’s tokenomics (maximum supply, circulating supply, issuance mechanics), holders’ rights as defined in the White Paper, YNG’s smart contract, or the terms of use on Young Platform and Uniswap.

And it is in no way a promise about price: an admission to trading is an infrastructure step, not an event that guarantees any market direction. We say this because we are the issuer, and a fact like this should always be put in its proper context.

This isn’t the last step

The WhiteBIT listing is part of a broader expansion of YNG’s trading venues that will continue through 2026. Young Platform continues to evaluate new trading venues for YNG. Any new announcements will be communicated to the public through an inside information disclosure pursuant to Art. 88 MiCAR, in line with the timing and requirements set out by the regulation.

On July 16 we launched YNG Boost (Vesting Service). What is it? Quite simply: by purchasing and locking Young (YNG) on the platform for 12, 24 or 36 months, you’ll receive an extra amount of YNG tokens (the Boost) added on top of what you’ve already purchased.

The best part? The more YNG you buy and the longer you lock it, the bigger the Boost — up to a maximum of 30%of the purchased amount! And that’s not all: there’s an additional Boost for members of our Clubs (Silver and above), up to 34.5% for Platinum Club members.

One important thing to keep in mind: selling and repurchasing YNG tokens you already hold excludes you from YNG Boost. As always, we recommend reading this article, which briefly explains how YNG Boost works: YNG Boost is here: buy Young (YNG), lock it, and get extra YNG tokens.

Interested in YNG Boost? Write to [email protected]: our team is happy to answer any questions.

This content constitutes a marketing communication for promotional purposes. Crypto-assets are high-risk, highly volatile instruments: their value can fluctuate significantly and may result in the loss of the capital invested. The information in this article is provided for informational purposes only and does not constitute financial advice or an investment solicitation. Past performance is not a guarantee of future results. Young Platform S.p.A. is the issuer of the YNG token pursuant to Regulation (EU) 2023/1114 (MiCAR); the current White Paper is available at https://storage.googleapis.com/young-documents/mica-whitepaper-YNG-token.xhtml.

Tap to Play, the first chapter of Arcade, has officially ended: what will happen in the coming days?

These have been intense days for everyone who participated in Arcade: Tap to Play, with Daily, Weekly, and Permanent Missions, the Championship, Tournaments, Leagues, and much more. Arcade, however, was far more than just a simple competition: it represented the natural conclusion of a journey that began a year ago with The Box, The Unbox, and The Reveal. In short, it was the vehicle to offer you a new way to experience personal finance, built on awareness and freed from constraints. On July 20th at 2:00 PM, the Arcade: Tap to Play Championship came to an end for good: in this article, we explain what lies ahead for you in the coming days.

Payment Account and Cashback in YNG

The first chapter of Arcade was deeply tied to the go-live of the Young Account*. Indeed, Tap to Play aimed to demonstrate that a new way of managing finances is possible: with Young Platform, you can manage your investments and personal finance—meaning Crypto and Cash—under a single, secure, transparent, and 100% compliant roof with Italian and European regulations, as proven by the acquisition of the MiCA license.

But that’s not all: if you are a member of our Clubs, by paying with the Young Card associated with your Payment Account, you are entitled to up to 3.6% Cashback in YNG on your daily expenses: do you spend €1,000 a month on groceries, clothes, restaurants, and more? If you are a Platinum member and use the Young Account, you will get €54 back in YNG tokens.

*Available only to residents of Italy

Communications and prize allocation: who won what?

As mentioned, Arcade ended on July 20th, and the final drawings for the Tickets of the last Tournament and the Leagues will take place in the following days, along with the official audit of the final leaderboard to calculate the gems.

Notifications to participants will start very soon: the top 20 players on the Championship leaderboard are about to receive their updates, and we will soon notify both the League winners (Diamond, Ruby, and Sapphire) and those who are holders of one of the drawn Tickets for Final Stage, the last Tournament.

If you don’t receive any notification right away, our advice is, of course, to wait until all updates have been dispatched. After that, if you still haven’t received any notification, you can easily open a ticket through ourSupport Center to request all the necessary information.

Those who won a physical prize will need to fill out a dedicated form to provide their shipping address, while winners of digital vouchers—such as Volagratis or Amazon ones—will receive the code to use directly via email.

Tournament Prizes (Tickets)

During the competition, we held three four-week Tournaments (Insert Coin, Checkpoint, and Final Stage) and one Special Tournament (Hall of Fame), each featuring exclusive prizes up for grabs like MacBooks, iPhones, and official Young Platform merch.

Throughout each tournament, you could collect Tickets based on the Gems accumulated by completing Missions. The final drawing, held in the presence of a notary, will determine the winning Tickets for this last tournament.

Gem Leaderboard Prizes (Championship) and Leagues

We would like to remind all participants of the prizes planned for the overall Gem Leaderboard of the Championship. The top twenty players will receive, based on their position, the following prizes:

1st: Rolex Oyster Perpetual 2023 green

2nd: Django Classic 125

3rd: MacBook Pro 14

4th: MacBook Air 13

5th: Volagratis GiftCard – value: €1,000

6th: iPhone 17

7th: Google Pixel 10

8th: Volagratis GiftCard – value: €700

9th: AirPods Max

10th: PlayStation 5

11th: Amazon GiftCard – value: €500

12th: Pixel Tablet

13th: Apple Watch Series 11

14th: Amazon GiftCard – value: €300

15th: Sony WH-1000XM5 Headphones

16th: Volagratis GiftCard – value: €250

17th: AirPods 4

18th: Amazon GiftCard – value: €200

19th: Volagratis GiftCard – value: €150

20th: Volagratis GiftCard – value: €120

Furthermore, players positioned from 1st to 2,000th place have been split into three Leagues (Diamond, Ruby, and Sapphire). Within each League, fantastic additional prizes will be drawn, regardless of your specific position. Specifically:

Diamond League (1st – 100th place)

1 experience at Villa Crespi with chef Cannavacciuolo

20 Young Platform hoodies

Ruby League (101st – 500th place)

40 Young Platform t-shirts

5 Forbes annual subscriptions

Sapphire League (501st – 2,000th place)

60 Young Platform caps

A special extra surprise prize

Speak to you soon!

We always recommend keeping an eye on the Young Platform app for updates on Tap to Play, but we will notify you as soon as the Final Stage Ticket drawings and League prizes are completed.

BNB is now on Young Platform: what it is, how it works and how to transfer your BNB to a MiCA-authorised European exchange.

Today’s listing is a big one: BNB officially joins the Young Platform catalogue. From today you can buy it, sell it, hold it in custody and — above all — deposit it directly from your wallets or from other platforms, without having to convert it into anything else.

What BNB is and what it is for

BNB is the native crypto-asset of BNB Chain, one of the most widely used blockchain ecosystems in the world. It was born in 2017 as an ERC-20 token on Ethereum before migrating to its own proprietary blockchain.

Today it is the native token of the BNB Smart Chain, a network compatible with the Ethereum Virtual Machine (EVM) — meaning it can run smart contracts and decentralised applications written to the same standards as Ethereum — based on a Proof of Staked Authority (PoSA) consensus mechanism, in which a limited number of validators, selected according to the tokens they have staked, produce the blocks, with fast confirmation times and low fees.

Within its ecosystem, BNB has clearly defined uses:

Network fees (gas): every transaction and every interaction with smart contracts on the BNB Smart Chain is paid for in BNB, just like ETH on Ethereum.

Staking and network security: holders can delegate their BNB to validators, taking part in the mechanism that keeps the network running.

Governance: those who stake BNB can vote on proposals to evolve the protocol.

BEP-20 token standard: BNB is the reference token for an ecosystem that hosts thousands of BEP-20 tokens, DeFi applications, the opBNB layer-2 solution, and the BNB Greenfield decentralised storage network.

A distinctive technical feature is the quarterly auto-burn mechanism: a portion of the BNB supply is periodically removed from circulation in a programmed, on-chain verifiable way, according to a public formula, with the protocol’s stated aim of reducing the overall supply over time. This is a structural feature of the token, not a guarantee of its value: the price of BNB remains determined by the market.

What changes from today: your BNB, wherever you want it

Until yesterday, anyone holding BNB who wanted to operate on the Young Platform had to sell or convert it elsewhere first. Not any more: from today, you can transfer your BNB as is, directly to your Young Platform account. Your BNB stays BNB — all that changes is where it is held.

And where it is held matters. Young Platform is a CASP authorised by Consob and the Bank of Italy under the European MiCA Regulation, with its registered office in Turin: a real address, in Italy, with European rules, transparency obligations towards clients and a supervisory authority to answer to. If part of your portfolio currently sits on platforms outside the European regulated perimeter, the BNB listing makes the transfer a simple operation: no sale, no conversion, no intermediate steps.

The right moment: the MYCA deposit promo runs until 2 August

There is one more reason to do it now. Until 2 August, the MYCA (Move Your Crypto Assets) promo is live, dedicated to anyone transferring funds to Young Platform: deposits in crypto — BNB included — and in euro count together towards the thresholds, starting from an overall value of €1,000.

The promo is structured in three Tiers (€1,000–9,999, €10,000–49,999, €50,000 and above), recalculated every week on the basis of net deposits, and unlocks growing benefits:

Bonus Wallet: a discount on trading fees, proportional to the amount deposited and usable until 31 December 2026;

Tax Report with a personalised discount of up to 70% off the list price;

Cashback in YNG tokens on everyday spending with the Young Card;

Payment account with a €0 fee for one year and a free Young Card;

Dedicated Account Manager for those in Tiers 2 and 3.

The full conditions, requirements and exclusions are set out in the MYCA promo Rules.

How to transfer your BNB to Young Platform

Log in to your Young Platform account (a completed KYC is required) and open the Deposit → BNB section.

Copy the deposit address and check the indicated network carefully: a transfer on an unsupported network may result in the loss of your funds.

Execute the transfer from the platform or wallet of origin. Upon on-chain confirmation, your BNB will be available in your Young Platform portfolio — and its value will count towards the calculation of your MYCA Tier.

For significant amounts, our support team can assist you step by step with the transfer.

Like every crypto-asset, BNB is subject to high volatility: its value can fall rapidly and significantly, potentially resulting in a total loss of the capital invested. BNB is not issued by Young Platform and its characteristics depend on a third-party protocol over which Young Platform exercises no control. Crypto-assets are not covered by bank deposit guarantee schemes or investor compensation schemes. Before operating, please read the General Risk Disclosure.

This is a marketing communication within the meaning of Regulation (EU) 2023/1114 (MiCA) and does not constitute investment advice, a personalised recommendation or a solicitation to purchase crypto-assets. Any decision to buy, sell or transfer crypto-assets is taken independently by the user.

BNB is a crypto-asset issued by third parties: Young Platform S.p.A. is not its issuer and is not responsible for the characteristics, evolution or functioning of the underlying protocol. Crypto-assets are highly volatile and carry a significant risk of loss, including the total loss of the capital invested; they are not covered by bank deposit guarantee schemes (Directive 2014/49/EU) or investor compensation schemes (Directive 97/9/EC). Past performance is not indicative of future results.

The MYCA promo is subject to terms, conditions and exclusions: before taking part, please read the full Rules. The promo benefits consist of discounts on fees and services and do not constitute returns on the crypto-assets deposited.

Crypto-asset services are provided by Young Platform S.p.A., Via F. Cigna 96/17, 10155 Turin, Italy — VAT no. 11931440017 — authorised by Consob and the Bank of Italy to operate as a Crypto-Asset Service Provider (CASP) under Regulation (EU) 2023/1114 (MiCA). For the contractual and economic conditions, please refer to the Information Sheets and the Terms & Conditions at youngplatform.com/legal.

With YNG Boost you buy Young (YNG), lock it for a period of your choice, and receive extra tokens up to 30%. The benefit increases further if you’re a Club member. Here’s how it works.

YNG Boost has arrived: the new Vesting Service for the YNG Token.

It works in a very simple way: you buy Young (YNG) at market price and agree to lock it on the platform for a period of your choice — 12, 24 or 36 months. In exchange, you receive an additional amount of YNG tokens, which is added to the amount purchased.

This is not a yield or interest: it is an amount of tokens distributed by Young Platform, as issuer, from its own treasury to support those who choose to stay and bet on the long term.

WARNING! Selling and repurchasing YNG tokens you already hold excludes you from YNG Boost. The Vesting Service applies only to new purchases. This is a simple rule with a precise purpose: to protect the token market, avoiding operations carried out solely to obtain the Boost — such as selling and repurchasing the same YNG — which could artificially alter its price and volumes. In addition, locked tokens cannot be used to access the Clubs.

How much extra YNG you receive

Your Boost depends on three variables that add up together: the amount of tokens purchased, the lock-up duration, and any Club membership.

Extra YNG share based on amount

Extra YNG share based on lock-up duration

You can choose to lock the Young (YNG) tokens purchased for 12, 24 or 36 months. The longer the lock-up period, the higher the boost percentage.

The two shares add together: combining the highest amount with the longest duration, the maximum boost reaches 30%.

In addition, the sum of the two YNG shares (by amount and duration) becomes the calculation base for further extra YNG based on the Club.

Club Premium YNG

If you have an active Silver, Gold or Platinum Club at the time of purchase, you receive a “Club Premium” calculated on the extra YNG for amount and duration (not on the capital):

This means that for a Platinum member — with a purchase of ≥ €250,000 and a 36-month lock-up — the total boost reaches up to 34.5%.

Keep in mind that, at the time of purchase, the Club level you belong to is taken as reference: if you change level afterwards, the bonus already assigned does not change.

Also, remember that the percentages indicate quantities of tokens, not percentages of return. The euro value of the purchased and additional YNG tokens can vary significantly over time, depending on market volatility.

Practical example

You buy €20,000 of YNG.

You choose a 24-month lock-up and are a Gold Club member.

The price of YNG is €0.50.

Here’s what you get:

YNG purchased: 40,000.

YNG by amount (+4%) = 1,600 YNG.

YNG by duration (+8%) = 3,200 YNG.

Total boost = 4,800 YNG

with Gold you add 10% = (10% x 4,800 YNG) → another 480 YNG.

The total? 5,280 extra YNG, in addition to the 40,000 already purchased.

YNG Boost: how it works in practice

You sign the contract for the Vesting Service

You buy YNG at market price on the platform.

We credit you with the additional YNG tokens.

Both the purchased and additional YNG are placed in vesting.

The purchased and additional YNG remain locked for the first 2 months (the so-called cliff): a technical period needed to complete the allocation.

From there on, month after month, a share unlocks automatically for the entire chosen duration, slower at the start, faster towards the end (exponential vesting).

You’ll find the list of tranches in the “Locked YNG” section of your Young (YNG) Wallet, tagged respectively as “VESTING – PURCHASED YNG” and “VESTING – ADDITIONAL YNG”.

When a tranche unlocks, you need to go into this section and click “Claim” to move the YNG to your main wallet and use it as you prefer.

Who can join

You need to complete KYC on the Young Platform and have residency in an EU member state (or an approved jurisdiction). Minimum amount: €5,000 per transaction. Valid only for new purchases: YNG tokens you already hold cannot enter the program.

How to join

The YNG Boost isn’t a button to press: before purchasing, you need to sign a dedicated contract. Just write to us at [email protected]: we’ll guide you from there, step by step. If you want to get an idea before writing to us, you can read the pre-contractual disclosure below.

Young (YNG) is the utility token issued by Young Platform, one of the few Italian platforms for the exchange of crypto-assets to have obtained MiCAR authorization and which has just closed a €22.5 million capital increase with Azimut as lead investor.

Today YNG is still, for the most part, a domestic market, with a predominantly Italian holder base; but its accessibility is progressively expanding beyond borders.

The token is already listed on Uniswap, the decentralized exchange where anyone, in any country, can trade it without intermediaries, while MiCAR authorization, with the European passport already active on the French market, opens the way to a wider user base across Europe. What today is mainly an Italian phenomenon could therefore move, in the coming years, towards an international market.

Risks to know

Like any crypto-asset, YNG is subject to price fluctuations, even significant ones: the value of the tokens you receive at the end of the lock-up period may be lower than what they are worth today. Furthermore, for the entire duration of the lock-up, the tokens are not available: you cannot sell or transfer them.

We remind you that no economic result is guaranteed. Crypto-assets do not benefit from bank deposit guarantee schemes or investor compensation schemes. You can find the full risk overview in the General Risk Disclosure and in the dedicated pre-contractual disclosure.

Tax aspects

Young Platform does not act as a withholding agent for income deriving from the Service: reporting and payment obligations remain your responsibility. To support you, Young Platform provides — in partnership with specialized professionals — tax advisory and reporting services for income tax returns, under the terms set out in the relevant Terms and Conditions. For your specific situation, consult a qualified accountant or tax advisor.

The Vesting Service is reserved for registered Young Platform users and is valid exclusively on new purchases of YNG at market price, with a minimum amount of €5,000 per transaction, subject to signing the relevant contract. The percentages of Additional YNG Tokens indicate quantities of tokens and do not in any way constitute a promise of return; their euro value can vary significantly depending on the token’s price performance. For the entire duration of the lock-up, the tokens are neither transferable nor usable and the transaction is irrevocable. YNG tokens are subject to market risk; the value of crypto-assets can decrease rapidly and you could lose the invested capital, in part or in full. Past performance is not indicative of future results.

This communication is a marketing communication pursuant to Regulation (EU) 2023/1114 (MiCAR) and does not constitute investment advice. Crypto-assets are not covered by the Deposit Guarantee Fund or by investor compensation schemes pursuant to Art. 38 MiCAR.

Young Group has completed a major €22.5 million capital increase led by the Azimut Group: a historic moment for Young Platform

Azimut, a group listed on the Milan Stock Exchange and a leader in public and private investment management and corporate financial services, has decided to back Young Group—the holding company that unites Young Platform and Fleap—with strong conviction. This is a fundamental moment in our history and for the future of innovation in Italy.

Young Group: crypto, digital banking, and real-world asset tokenisation

Those who have followed us from the very beginning know well that Young Platform and its ecosystem were born out of a very clear desire: democratise and simplify access to the world of crypto-assets.

This mission took shape from the vision of a group of students from the Polytechnic University of Turin who, driven by a passion for innovation and technology, decided to turn this idea into reality.

Today, nearly ten years later, Young Platform represents a safe, reliable, and transparent routeto the world of crypto-assets for hundreds of thousands of investors, both in Italy and abroad. All of this is further strengthened by the recent acquisition of the MiCA authorisation, a seal of guarantee issued by Italian and European regulators, officially certifying our platform’s total compliance with current regulations.

Over time, however, we wanted to widen our scope, focusing also on a blockchain-related trend destined to revolutionise the global financial system: the tokenisationof real-world assets (RWA, Real World Assets). How? By integrating Fleap into our ecosystem, the first Italian company to obtain authorisation from CONSOB (the Italian National Commission for Companies and the Stock Exchange) for the digitalisation and tokenisation of financial instruments such as shares, bonds, and debt securities.

It is for these reasons that Young Group was born—a holding company based in Turin, created specifically to bring these two souls under one roof and, ultimately, build an increasingly complete, cross-sectional, and efficient infrastructure.

Azimut supports Young Group with a €22.5 million investment

The Azimut Group believes in the future of this project and has demonstrated this by leading a €22.5 million investment in Young Group as the lead investor. This is because, as highlighted by CEO Giorgio Medda, the Azimut Group’s strategy “has long been looking closely at the evolution of financial markets and the role of digital assets and blockchain technologies” and Young Group, in this sense, “is a solid business project, fast-growing, and distinguished by significant technological expertise and a strong focus on security and regulatory compliance.”

But, to fully grasp the scope of this event, it is helpful to understand who Azimut is: we are talking about an independent, global group, a leader in asset management across public and private markets, wealth management, and investment banking. It is a companylisted on the Milan Stock Exchange, present in as many as 20 countries worldwide, and backed by a network of around 2,000 professionals, including fund managers and financial advisors.

What does this capital increase mean for Young Platform?

Andrea Ferrero, our Co-CEO and co-founder, answered this question very clearly: “The investment marks a new phase in Young Group’s growth path and strengthens our ability to execute a vision we have pursued since our inception: build a financial infrastructure where crypto-assets, banking services, and tokenised assets coexist in a single, simple, regulated, and accessible experience.”

In this new chapter that is about to open, we would like to make one thing clear: our identity is and will always remain community-focused—on those who have never stopped believing in Young Platform.

The beating heart that binds our supporters together is Young (YNG), the utility token required to make the most of the platform’s features, designed to intimately reflect the growth and performance of the entire ecosystem. In other words: the more Young Group expands and strengthens,the more solid the foundations on which the YNG token rests become.

Fasten your seatbelts: a new adventure begins

To conclude, with this €22.5 million capital increase, Young Group enters a new era: the continued support of institutional partners of Azimut’s caliber allows us to raise standards and accelerate development, enhancing the ecosystem through three fundamental pillars:

Crypto: with an increasingly efficient Young Platform and the Young (YNG) token at the core of the project;

Digital Banking: through the Young payment Account and Card;

Real World Assets: thanks to the digitalisation and tokenisation infrastructures offered by Fleap.

We have dreamed big since day one, and today we have the tools, the capital, the licenses, and, most importantly, the right community to drive our goals forward. We are ready to begin a new phase of our history—are you with us?

Before we start: what is MiCAR and why does it matter to you?

MiCAR (which stands for Markets in Crypto-Assets Regulation) is the unified European regulation that, from 30 June 2026, governs the operation of crypto platforms across the European Union. To draw a comparison, it is very similar to the banking regulations introduced in the 2000s: a set of harmonised rules defining how crypto platforms must treat customers, custody their assets, disclose risks, and manage conflicts of interest and complaints.

Young Platform was authorised as a CASP (Crypto-Asset Service Provider) by Consob and Banca d’Italia on 30 June 2026. From that date, we have updated our entire platform to comply with these rules. This guide explains — in practical terms — what has changed from your perspective as a customer.

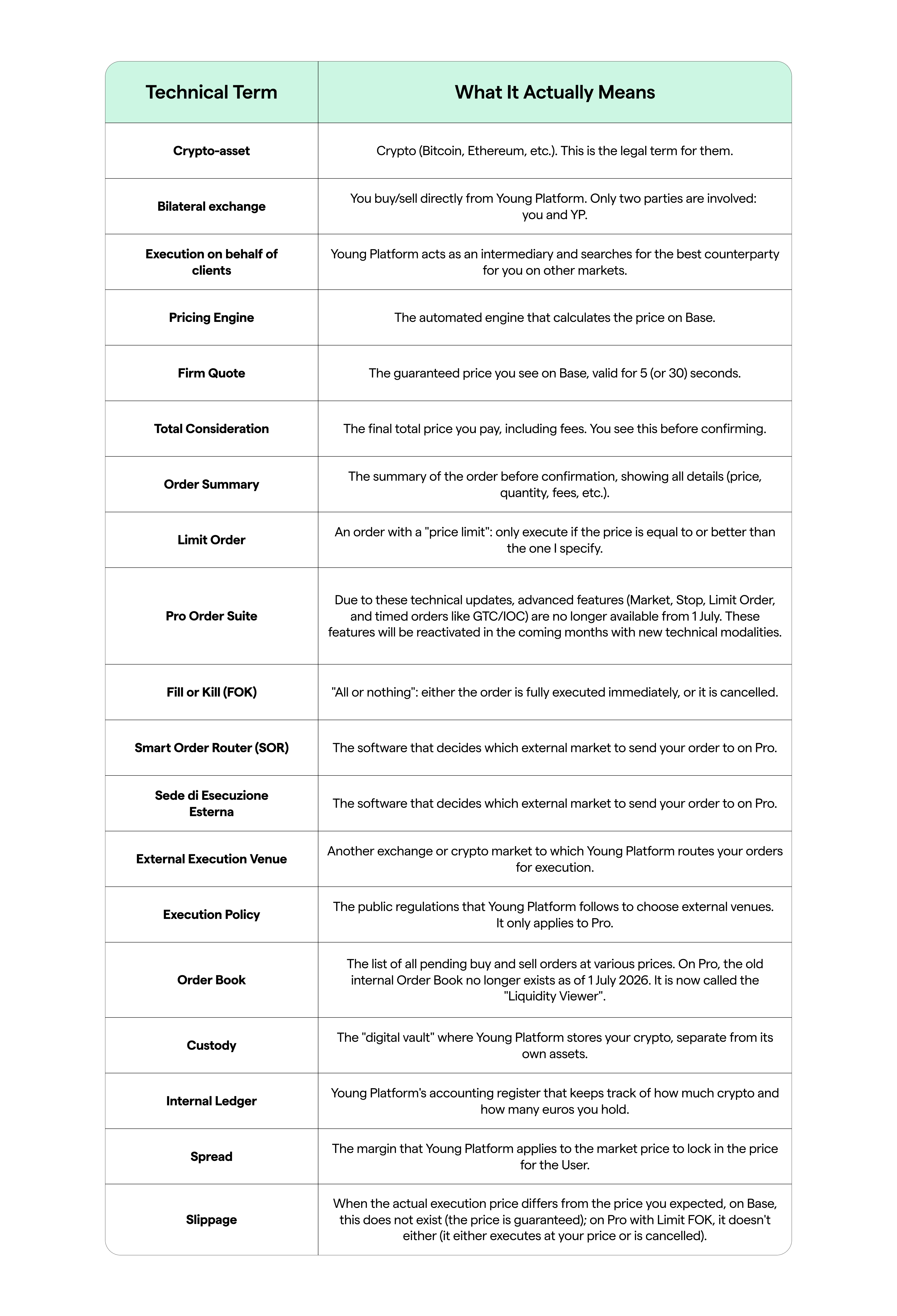

If you have already read our “Base vs Pro” guide, you will find the other updates here. If you haven’t read it yet, we highly recommend doing so first. You can find the link here: Guide to understanding Young Platform Base and Young Platform Pro post-MiCAR. Concepts such as Bilateral Trade, Execution Policy, Order Book, and Limit Orders apply here too.

1. The YNG Token will temporarily only be available on Base, not Pro

What has changed

Prior to 1 July 2026, you could buy and sell the YNG Token (Young Platform’s proprietary token) on both Young Platform Base and Young Platform Pro. Since 1 July 2026, it has been available only on Base. It is no longer possible to place buy or sell orders for YNG on the Pro platform. All pending YNG orders on Pro were automatically closed during the maintenance window on the night between 30 June and 1 July, and your Euro/crypto funds were returned to your available balance.

Please note: Any YNG holdings you had in your “vault” (custody) have not been affected. If you had 500 YNG in your wallet, they are still there. Only the way you buy and sell them has changed: from now on, you will do this on Base.

Why

On the Pro platform, Young Platform acts as an intermediary, sourcing the best counterparty across external markets (other exchanges). However, the YNG token is not yet admitted to trading on other qualified external exchanges connected to Young Platform. Consequently, there was effectively no external market for it on Pro.

What you need to do

If you previously used Pro to buy or sell YNG, you must now use Base (either via exchange.youngplatform.com or the updated mobile app). The process remains the same: you see the price, you have 5 seconds to accept it, and the transaction is settled directly with Young Platform.

This service may return to Pro in the future, if and when YNG is admitted to trading on external qualified exchanges. Young Platform will notify you well in advance if this happens.

2. Withdrawals and deposits: new transfer verification rules

This is likely the most noticeable update for anyone transferring crypto between Young Platform and external wallets. The rules vary depending on where the crypto is going (or coming from) and the amount involved.

The golden rule (always applicable): you can only transfer to your own wallets

First and foremost, this is the most critical rule to remember, and it applies to any transaction amount, without exception: you cannot send crypto from Young Platform to a non-custodial wallet (such as MetaMask, Ledger, Trezor, etc.) registered to someone else. This applies even if they are your parent, sibling, best friend, or a merchant. The same rule applies to incoming deposits: if crypto enters your Young Platform account from a non-custodial wallet, that wallet must belong to you, not a third party.

This restriction stems from the European Travel Rule Regulation (Regulation EU 2023/1113) and applies regardless of the monetary value: even a €5 transfer is prohibited if the destination non-custodial wallet cannot be proven to be yours. If you attempt this, the platform will block the transfer, and your crypto will remain held until the transaction is cleared.

For wallets held with other authorised exchanges (e.g., Coinbase, Kraken, etc.), specific checks are also carried out.

How Young Platform verifies that a non-custodial wallet is actually yours

A non-custodial wallet is one where only you hold the private keys. Examples include MetaMask, Ledger, Trezor, Trust Wallet, and Rabby. The way Young Platform verifies ownership depends on the transfer amount.

If the amount is under €1,000: A dedicated screen will appear where you must tick a box declaring, under your own responsibility, that you are the sole owner of the wallet and the private keys. This is a legally binding self-declaration: declaring false information carries personal liability. Without ticking this box, the transfer cannot proceed.

If the amount is €1,000 or more: Self-declaration is no longer sufficient. You will be asked to provide a formal cryptographic signature. This is required to objectively prove — rather than just declare — that you possess the private keys to that wallet.

What “cryptographic signature” means in simple terms

A cryptographic signature is a mathematical signature. It is not a written declaration, but a technical process: it involves using your wallet’s private keys to sign a unique message sent to you by Young Platform. If you are the genuine owner of the wallet, you will be able to generate this signature. If you are not, you won’t. It is the equivalent of proving you own a car by not just showing the logbook, but actually starting the engine with your key in front of a notary.

The practical steps on your screen are fully guided:

Young Platform displays a message.

You open your non-custodial wallet.

Your wallet prompts you to confirm the signature (usually via Face ID, PIN, or by tapping your Ledger/Trezor hardware device).

Your wallet generates the signature and transmits it to Young Platform.

If the signature is valid, Young Platform releases the transfer. If it is invalid (or if you do not complete it), the transfer will be rejected and your crypto will remain in your Young Platform account.

The technical service provider Young Platform uses to manage this signature verification is Notabene, a platform specialising in Travel Rule compliance.

If the wallet is on another exchange

In this case, the logic is different. A wallet on another authorised exchange does not have “private keys” that the customer can sign — the hosting exchange holds them. Therefore, cryptographic signing does not apply.

Instead, the Travel Rule requires an automatic exchange of data between Young Platform and the destination exchange. Specifically:

When you set up the transfer, Young Platform will ask you for the recipient’s personal details (first name, surname, and whether they are you or someone else).

Young Platform and the receiving exchange will automatically and securely exchange this data in an encrypted format using an international technical standard called IVMS101 (essentially a “common language” for crypto platforms).

If the other exchange confirms the details, the transfer goes through.

If the other exchange does not respond or provides incomplete data, the transfer will be temporarily held, and Young Platform will ask you to manually provide the missing details before releasing it.

Once again, Notabene is the technical tool orchestrating this secure data exchange between platforms.

What is the Travel Rule (and why does it exist)?

The Travel Rule is a regulatory standard introduced by the European Union under Regulation EU 2023/1113. Essentially, it dictates that specific identifying data must “travel” with the transaction, just as it does with international bank transfers. If a bank processes a €10,000 transfer to another bank, it must specify the sender and the recipient — name, address, and IBAN. The crypto Travel Rule operates in the same way, with minor technical adjustments (using blockchain addresses instead of IBANs).

The objective is to prevent money laundering and terrorist financing: by ensuring every crypto movement is traceable, it becomes significantly harder to move illicit funds through regulated platforms.

What happens if a transfer gets blocked?

This can happen for several technical reasons:

The receiving exchange fails to respond to the data exchange promptly.

The sent data is incomplete.

Your non-custodial wallet fails to sign due to a technical error.

The destination address is flagged on a suspicious list (such as sanctioned addresses, known scams, etc.).

In all these scenarios, the transfer goes into a temporary block. Your crypto will not leave your account and will not reach the recipient until the issue is resolved. You will receive an in-app notification explaining what is missing and what you need to do (for example, providing the signature again, updating the recipient’s details, or contacting Customer Support).

Please do not worry if this happens: it is a protective security mechanism, not a penalty. If you have any doubts, get in touch with Customer Support straight away.

What is the Transfer Policy (in a broader sense)?

It is worth distinguishing between two documents that sound similar but cover different areas:

The Crypto-Asset Transfer Policy (Article 80 MiCAR) is the document where Young Platform outlines how it delivers its transfer services as a regulated activity: who is permitted to make transfers, how transfers are processed, what technical security measures are in place, and so on.

The Travel Rule Procedure (Regulation EU 2023/1113) is a more specific document detailing how Young Platform collects and exchanges the data that must accompany every crypto transfer, and how it implements cryptographic signatures for non-custodial wallets.

These two documents are designed to be read alongside each other.

What you need to do in practice

If you are transferring less than €1,000 to or from your own non-custodial wallet: Simply tick the self-declaration box when prompted. That is all.

If you are transferring €1,000 or more to or from your own non-custodial wallet: Be ready to perform the cryptographic signature (make sure your wallet is open on your phone or your hardware device is connected beforehand).

If the wallet is on another exchange: Provide the requested personal details; the rest is handled automatically in the background.

Never attempt to send crypto to another person’s non-custodial wallet (not even a family member): this is strictly prohibited at any transaction value. If you need to send crypto to someone, ask them to set up their own account on Young Platform or another authorised exchange.

3. Delisting: some cryptocurrencies are no longer available

What happened

With the introduction of MiCAR, Young Platform had to review the list of available cryptocurrencies on our platform. Some have been removed. The technical term for this is “delisting”, which simply means removing them from our available selection — much like a supermarket taking certain products off the shelves if they no longer meet new regulatory standards.

Why

The reasons vary depending on the specific crypto-asset:

Some stablecoins do not hold EMT (E-Money Token) status under MiCAR and therefore cannot be offered within Europe. USDT (Tether) is the most prominent example: as it is not yet compliant with MiCAR, it cannot be marketed as an EMT within the EU.

Some crypto-assets are deemed high-risk due to low liquidity, technical vulnerabilities, or concerns over project governance.

Some crypto-assets lack a MiCAR-compliant White Paper notified to the relevant competent authority, which is now a mandatory requirement for offering assets to the European public.

The fully updated list of supported cryptocurrencies is always available to view at youngplatform.com/en/exchange/listed/ and in our Terms and Conditions.

What you need to do

If you were affected, you will have received a dedicated notice from Young Platform outlining your options (such as converting the assets, withdrawing them to an external wallet, etc.) along with a deadline. If you don’t remember receiving this email, please check the email address associated with your account. If you have any questions, contact Customer Support.

4. Some trading pairs are changing: from USDC to EUR

What is a trading pair?

A trading pair (or “pair”) is the combination of two assets you are exchanging. If you buy Bitcoin using Euros, the pair is BTC/EUR. If you buy Bitcoin using USDC (a dollar-pegged stablecoin), the pair is BTC/USDC.

What has changed

Following 1 July 2026, Young Platform converted several trading pairs from USDC to EUR.

Why

There are two main reasons for this:

It is simpler for you: When you buy using EUR, you know exactly how much you are spending in your local currency. Buying in USDC requires extra mental steps (converting Euros to USDC, then USDC to BTC), and each step carries a small transaction cost. For European retail users, EUR pairs are far more intuitive.

Regulatory requirements: Under MiCAR, offering pairs against stablecoins that must meet specific criteria (authorised EMTs) involves stricter checks and disclosure requirements. In some cases, for operational efficiency, it is preferable for Young Platform to support the trading pair directly in Euros.

What you need to do

If you used to trade regularly against USDC on certain cryptocurrencies, check if the pair has switched to EUR. If it has, there is no cause for concern: you can continue making the same trade; you will simply pay and receive Euros instead of USDC. If you still require USDC, you can buy it separately just like any other cryptocurrency.

5. Moneybox (recurring purchases) and Recurring Staking

What is the Moneybox?

The Moneybox feature allows you to set up automatic, recurring purchases (weekly, bi-weekly, or monthly) for one or more supported cryptocurrencies.

These recurring Moneybox purchases are built on the same Bilateral Trade model described in our “Base vs Pro” guide. We have included a brief summary below, though we highly recommend reading the full guide.

What has changed

Quite simply, when you tap “Buy”, you are purchasing crypto directly from Young Platform. The platform acts as the sole dealer: Young Platform sells to you (or buys back from you) the cryptocurrency at the price displayed on your screen.

When setting up a recurring purchase plan via Moneybox, you will be asked for prior authorisation to execute these orders. This is designed to automate and simplify the recurring purchase process.

When a recurring purchase is executed through Moneybox, Young Platform applies a 1.89% fee on the transaction value for orders exceeding €100. For a complete overview of our fees, please visit this page.

Naturally, you can edit, pause, or cancel your Moneybox plan at any time, which will apply to all future scheduled orders.

What is Recurring Staking?

Recurring Staking allows you to schedule automatic purchases of crypto (on a weekly, bi-weekly, or monthly basis). Once purchased, the crypto goes straight into your Staking Wallet — which we will cover below — to start generating rewards automatically, with no further action required from you.

As with the Moneybox, purchases made through Recurring Staking follow the Bilateral Trade model.

What has changed

Each scheduled purchase via Recurring Staking works exactly like those authorised under the Moneybox feature: you buy the crypto directly from Young Platform at the real-time calculated market price, with fees following the same structure linked above.

As soon as the purchase is complete, the crypto is instantly moved into your Staking Wallet. We discuss this in more detail in the next section, but please keep in mind that, from a legal perspective, the Staking service is governed by its own contract and is not regulated under MiCAR.

By activating the plan, you authorise both the purchase and the transfer to your Staking Wallet in advance, with all costs clearly outlined from the start. Just like the Moneybox, you can modify, pause, or cancel your plan at any time. Any changes will apply starting from the next scheduled purchase.

If you cancel one or more stakes, any funds you have already accumulated will be automatically moved back to your Main Wallet.

The Staking Wallet is not a MiCAR-regulated service

What is the Staking Wallet?

The Staking Wallet is a service on Young Platform that allows you to “stake” certain cryptocurrencies (such as Ethereum) to receive periodic rewards. Technically, when you stake, your crypto is “locked” to help support the operations of the blockchain, and in return, you earn rewards over time.

Why we want to clarify that “it is not a MiCAR service”

Simply because MiCAR does not directly regulate staking. The European regulation covers activities such as exchanging crypto-assets (Article 77), executing orders on behalf of clients (Article 78), custody (Article 75), transfers (Article 82), advice, discretionary portfolio management, and placement. Staking as a standalone service is not covered.

This leads to two key practical implications:

MiCAR protections (such as custody asset segregation, risk disclosures, and provider requirements) apply to the underlying custody service, not to the staking service itself.

Staking carries specific risks that are not covered by the MiCAR framework, which you should be fully aware of before activating it. These include slashing risk (where a portion of your staked crypto can be confiscated if the validator makes an error), protocol risks (for example, Lido for Ethereum), potential lock-up periods during which you cannot withdraw, and de-pegging risks for derivative tokens like wstETH (Wrapped Staked Ether).

What you need to do

If you use the Staking Wallet, please carefully read the specific Terms and Conditions of the Staking Wallet and the dedicated risk disclosures published at youngplatform.com/staking-wallet/. These are separate from Young Platform’s General MiCAR Terms and cover specific details such as:

How rewards are calculated.

When you will receive them.

Which cryptocurrencies are staked and with which protocols/validators.

How the “unstaking” (withdrawal) process works.

What happens in the event of protocol slashing or technical issues.

In summary: The Staking Wallet is just as secure as before, but it is a distinct service from MiCAR-regulated services, governed by its own rules and risks. Please treat it as such.

Key takeaways in a nutshell

If you only remember the most practical points from this guide, make sure they are these:

YNG can only be bought and sold on Base, no longer on Pro.

Transfers to non-custodial wallets: Only to your own wallet (never to third parties, regardless of the amount). For amounts under €1,000, a self-declaration checkbox is enough; for €1,000 and above, a cryptographic signature is required. If the wallet is on another exchange, personal data is exchanged automatically via Notabene (Travel Rule).

Certain cryptocurrencies have been removed from the platform. If you held any of these, you have already been notified of your options.

Some trading pairs have changed from USDC to EUR, improving price transparency.

The Staking Wallet and the DeFi Wallet are not MiCAR services. They have their own rules and risks: make sure to read their dedicated disclosures.

Questions & Answers

1. Do I need to download a new app for the cryptographic signature?

No. If you already have a non-custodial wallet (such as MetaMask, Ledger, Trust Wallet, etc.), you will perform the signature directly within that wallet. If you do not have a non-custodial wallet and only want to transfer crypto to accounts on other exchanges (like Coinbase or Kraken), you do not need one: you will simply follow the “proof of account ownership” procedure.