Laziness is a virtue in the investment world! Discover five other paradoxical and counterintuitive (but true) assumptions from the world of personal finance.

What are the central paradoxes of personal finance? Our blog primarily focuses on cryptocurrencies but occasionally explores other areas of the vast investment landscape.

Recently, we came across an intriguing article by Dedalo Invest. The author, Andrea Gonzali, outlines personal finance’s 10 contradictions (or paradoxes). We decided to revisit this article because many of its points resonate strongly with the crypto world.

The investment world can often be counterintuitive.

While the primary goal of those exploring the markets is logical—maximising returns and minimising losses—many investor actions can seem irrational, especially without the benefit of hindsight. In summary, the objective is clear, intuitive, and rational, but its methods can be complex.

There isn’t a single reason for this complexity. Historically, humans have developed intuition for two key purposes: to ensure the survival of our species and to perpetuate it through procreation. This focus does not include increasing financial capital. To quote the original article’s author, “The fundamentals are intuitive: save regularly, invest wisely, diversify your portfolio, and maintain it over the long term. It is the management of money that is complex.“

Laziness is a virtue.

Let us start with perhaps the most paradoxical statement: laziness often maximises performance, while hyperactivity tends to hinder it. Of course, this observation is not meant to generalise; exceptions certainly exist, such as the highly active meme coin trader who is our friend’s cousin. However, when analysing broader investment and personal finance trends, many of society’s beliefs about the value of hard work and commitment are challenged.

It is essential to clarify that in this context, laziness refers specifically to the operational side of investing, such as the frequency of buying and selling or rebalancing, rather than the time spent studying concepts or theories. This idea also applies to the world of cryptocurrency. The more trades one makes in a particular timeframe, the greater the risk of making mistakes that can lead to significant losses, especially when dealing with certain types of cryptocurrencies.

In traditional finance, so-called “lazy portfolios”—portfolios that simply diversify among a few asset classes using financial instruments that require minimal intervention—have historically outperformed many more complex, actively managed strategies. The same can be said for portfolios predominantly composed of Bitcoin and a few altcoins, even over shorter investment horizons.

Several reasons account for this phenomenon. First and foremost, every trade made on a brokerage platform or a crypto exchange incurs costs and increases the likelihood of making errors. Due to the unpredictable nature of the markets, even professional investors do not try to time the market effectively—that is, they do not attempt to sell assets at their peak value or buy them at their lowest point. Finally, it’s important to note that any capital gains realised from trading are subject to taxation.

You have to follow your intuition

Intuition is crucial for our safety, alerting us to danger before it becomes apparent. However, relying on intuition can be risky when it comes to investments. While humans have only recently begun investing their money, our intuition and the cognitive biases linked to it have developed over hundreds of thousands of years. In simpler terms, our intuition evolved to protect us from threats like wild animals or poisonous plants, not to navigate the complexities of the post-Trump trade market crash.

These cognitive biases are mental shortcuts that shape our beliefs and influence quick decision-making, significantly affecting our investment choices:

1. Anchoring: We assign excessive and irrational value to specific price points. A notable example is the $100,000 threshold for Bitcoin, where many investors made mistakes during the 2021 bull market because they believed BTC would reach this level.

2. Overconfidence Bias occurs when we overestimate our knowledge, decision-making abilities, or predictions’ accuracy.

3. Confirmation Bias: This bias leads us to selectively seek information supporting our existing opinions while ignoring data that contradicts them.

For this reason, rigid investment approaches characterised by clear, unbreakable rules—such as a recurring and buy-and-hold strategy—tend to yield better results than those based on an investor’s instincts or subjective perceptions.

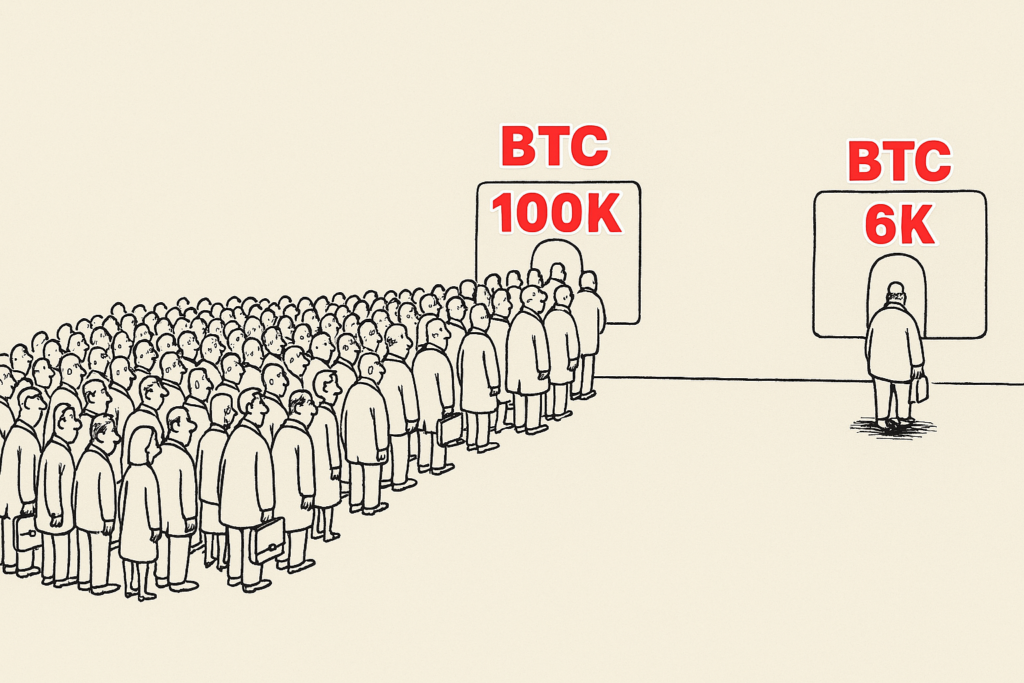

Sales do not attract buyers.

In finance, especially in cryptocurrency, a price decline often drives buyers away, contrary to what typically occurs in other markets. For instance, if we are interested in a pair of shoes and their price drops by 50%, we will likely welcome this reduction and make a purchase. This creates a paradox where, in the markets, the opposite behavior is observed. The well-known meme illustrating a long line of buyers when Bitcoin’s price is $100,000 and an empty line when it falls to $6,000 effectively captures this reality.

The herd effect can explain the concept: when everyone is selling, our instinct prompts us to follow suit, even though we know rationally that it might be the best time to buy. Discounts can be intimidating in the markets because falling prices are typically linked to negative news or behaviors, altering the perception of investors anticipating further declines.

Investing near the highs is the norm, not the exception.

Let’s shift our focus from the crypto sector to traditional financial markets, particularly the stock market. This shift isn’t because the concepts we’re discussing are exclusive to traditional markets but because crypto assets are relatively young compared to stock indices. As a result, we have insufficient historical data to support our thesis fully.

Those entering the investment world for the first time often fear buying at market peaks or feel they are entering too late. However, this concern is unfounded mainly when we examine the history of the S&P 500, the leading stock index that tracks the performance of the 500 largest companies in the United States and, in many ways, reflects general market trends.

The S&P 500’s chart, which begins in 1957, shows that it spends a significant amount of time near its all-time highs. Between 1957 and March 2025, the index recorded 1,242 new highs. Typically, these all-time highs are separated by very short periods, although there have been a few notable exceptions, such as the seven-year gaps between 2000 and 2007 and between 1973 and 1980.

In summary, reaching new all-time highs in traditional finance is not an extraordinary event but the norm.

The notion that investing during a bearish market is easier is often misleading. When markets collapse, fear and uncertainty prevail, making investing paradoxically more challenging, even when prices are significantly lower.

What about the world of cryptocurrency? Currently, Bitcoin cannot be compared to the S&P 500 due to the 50-year history that separates them. This difference contributes to Bitcoin’s value being more cyclical and subject to volatility. However, Bitcoin has recently reduced the time between reaching all-time highs, likely due to increased interest from institutional investors. Over time, although we cannot be sure, Bitcoin’s price movements will probably start to resemble those of traditional assets, with gold being a prime example, as both share the characteristic of scarcity.

Investing near the highs is the norm, not the exception

We arrive at the fifth and final point, aptly summarised by Daedalus Invest, in the following paradox:

- It is essential to start investing as early as possible to benefit from compound interest.

- However, you cannot act blindly; you must fully understand what you are doing and educate yourself before you begin investing.

The first statement is straightforward if you know how compound interest works. It refers to the percentage return you earn on an amount that includes previously accumulated interest—essentially, it’s interest on interest. Nevertheless, jumping in without a solid foundation of knowledge can lead to mistakes that may be costly and disheartening, prompting individuals to step away from investing altogether.

So, how can you overcome this challenge? Start by exploring the wealth of resources available on our Academy and Blog!