Bitcoin’s price surges on Chinese economic stimulus measures and strong ETF inflows. What’s next for Bitcoin this October?

Bitcoin has recently shown a surprising upturn, closing September with an impressive 8% increase. This performance defies the usual trend, as September is typically a weak month for the cryptocurrency. The drivers behind this growth are strong ETF inflows and significant liquidity injections from China, which have sparked optimism across global markets.

China Injects Capital and Cuts Repo Rates

Last Wednesday, China’s central bank announced a reduction in its interbank lending rates (repo rate) from1.95% to 1.85%, complemented by a $10 billion liquidity injection and a 50-basis-point cut in the required reserve ratio (RRR) for banks. This move appears to be part of a larger economic stimulus package aimed at revitalising the economy with an anticipated ¥1 trillion (around $150 billion) in increased credit availability for banks.

This intervention seeks to counteract key economic challenges, including deflation driven by low consumer demand, a struggling real estate market, and high public debt. The effects have been immediate, with Asian stock indices like Hong Kong’s Hang Seng and Shanghai’s SSE surging 14% and 20%, respectively, since Thursday. This positive momentum also boosted the U.S. and crypto markets, although Bitcoin and other major cryptocurrencies have since eased, with BTC down by about 3% today.

China’s liquidity boost not only lifted Asian financial markets but also generated optimism among global investors. The repo rate cut and other measures are expected to increase the global money supply, with many analysts speculating that a portion of this liquidity may flow into riskier assets, including stocks and cryptocurrencies, in the coming weeks.

Impact on Investor Sentiment and Bitcoin’s Price

Bitcoin’s recent price surge is also tied to rising inflows into Bitcoin ETFs, further strengthening investor confidence. Last Friday, ETF inflows reached nearly $500 million, a level not seen since July. This significant capital flow into Bitcoin funds suggests renewed market optimism after prolonged stagnation.

Ethereum has also shown promising signs, with ETF inflows totalling $150 million over the past four trading days. This uptick comes after two challenging months for Ethereum ETFs, hinting at a potential shift in sentiment for the broader crypto market.

Will October Bring Renewed Momentum?

Despite minor pullbacks over the past 24 hours, optimism persists across markets. As we enter October, a historically bullish month for Bitcoin (often dubbed “Uptober”), will this mark the beginning of a sustained uptrend after over six months of sideways movement?Download the Young Platform app to stay updated on Bitcoin’s market dynamics and the global economic factors influencing cryptocurrency prices. Follow our weekly updates to stay ahead in the world of crypto investing.

Discover the 10 most iconic Japanese cars, from the Toyota Supra to the Nissan GT-R. Explore the models that have shaped automotive history.

Japanese cars have made an indelible mark on the automotive world, combining cutting-edge technology, dependability, and remarkable performance. Since the 1960s, Japanese car brands have set new industry standards, from efficient compact cars to high-performance supercars. Here, we highlight 10 of the most iconic Japanese import cars, each leaving its own legacy and captivating car enthusiasts worldwide.

10. Honda Civic Type R

The Honda Civic Type R stands out among Japanese cars for its compact, sporty design and impressive power. Equipped with a 2.0-litre turbocharged VTEC engine, it delivers over 300 horsepower, making it a favourite among those who seek a dynamic driving experience. First launched in 1998, the Civic Type R has established itself as a benchmark in the hot hatch category.

9. Mazda MX-5 Miata

The lightweight Mazda MX-5 Miata has become a legend in the world of Japanese roadsters. Launched in 1989, it combines sleek design, agile handling, and rear-wheel drive, offering a pure and exhilarating driving experience. This iconic Japanese import car has sold over a million units worldwide, making it one of the best-selling roadsters in history.

8. Toyota Supra

The Toyota Supra, especially its fourth-generation (A80) model introduced in 1994, is a legend in its own right. Its 3.0-litre 2JZ-GTE twin-turbo engine offers exceptional tuning potential, easily reaching over 1,000 horsepower with modifications. Known for its smooth styling and power, the Supra has an enduring fan base among performance enthusiasts and is a hallmark of Japanese cars.

7. Nissan GT-R

Dubbed “Godzilla,” the Nissan GT-R R35 is a supercar killer that has shaken up the automotive world since its release in 2007. With a 3.8-litre twin-turbo V6 engine and an advanced all-wheel-drive system, the GT-R competes with European supercars at a fraction of the price. The GT-R’s predecessor, the R34 Skyline, remains an icon among Japanese import cars due to its legendary RB26DETT engine and cult status.

6. Subaru Impreza WRX STI

Famed for its success in rally racing, the Subaru Impreza WRX STI features a turbocharged 2.5-litre boxer engine paired with an advanced all-wheel-drive system. Known for bringing rally-level performance to everyday roads, it’s a top choice for those who love the thrill of the drive. This model is a prime example of the innovation that Japanese car brands bring to the world of sports cars.

5. Lexus LFA

The Lexus LFA is a limited-edition supercar powered by a 4.8-litre V10 engine developed in collaboration with Yamaha. Its carbon fibre construction, along with its distinctive engine sound, makes it a true masterpiece in Japanese cars. Despite its high price, the LFA is celebrated as one of the best supercars of the 21st century, combining exclusivity with unmatched performance.

4. Mitsubishi Lancer Evolution

The Mitsubishi Lancer Evolution, known as the Evo, is a high-performance sedan with a turbocharged engine and all-wheel drive. First launched in 1992, it quickly became a rally legend and a favourite among Japanese import cars enthusiasts. Known for its accessibility and impressive performance, the Evo remains a symbol of Japanese car brands dedicated to high-performance engineering.

3. Nissan 350Z / 370Z

The Nissan Z series, particularly the 350Z and 370Z models, are known for their aggressive styling and powerful V6 engines. As part of a long lineage of Z-cars, these models continue the tradition of Japanese sports cars, appealing to both pure driving enthusiasts and tuning fans. The 370Z is especially valued as an affordable yet spirited sports car.

2. Honda NSX

Introduced in 1990, the Honda NSX was Japan’s first supercar, featuring a mid-mounted V6 engine and an aluminium body. Developed with input from legendary F1 driver Ayrton Senna, the NSX redefined supercars by offering high performance with a level of reliability uncommon in its category. Its influence on both design and engineering remains significant among Japanese car brands.

1. Toyota 2000GT

Often regarded as Japan’s first true sports car, the Toyota 2000GT was produced in limited quantities between 1967 and 1970. With a sleek design and a six-cylinder engine, it put Japan on the map in the world of sports cars. Today, the 2000GT is a rare and highly prized collector’s item, embodying the elegance and quality for which Japanese car brands are celebrated.

Why Are Japanese Cars So Popular?

Japanese cars are renowned for their reliability, performance, and value. Models like the Toyota Supra and Nissan GT-R have redefined what sports cars can offer, while the Honda NSX and Lexus LFA have challenged European supercars with impressive success. The commitment to quality and technological innovation across Japanese car brands makes these vehicles not just means of transport but engineering marvels.

The €2.65 million capital injection “on top” from Azimut and the appointment of new president Nicolas Bertrand, a senior executive at Borsa Italiana and the London Stock Exchange.

Milan, September 16, 2024 – Azimut, a leading independent asset management group in Europe with over €95 billion in assets under management, has strengthened its support for Young Platform through an additional €2.65 million capital investment. This new funding is an extension of Azimut’s prior investment of €11 million in June 2022, when it led a €16 million funding round.

Young Platform, the Italian fintech scale-up focused on democratising access to the cryptocurrency space, now boasts over 2 million registered users. Known for its extensive range of crypto services, Young Platform is positioned as a leader in Italy and well-prepared to tackle new challenges and introduce innovative products.

As part of this new phase, Young Platform has appointed Nicolas Bertrand, a seasoned executive from Borsa Italiana and the London Stock Exchange Group (LSEG), as its new president. This addition to the leadership team aligns with the company’s commitment to regulatory alignment and sustainable growth.

Further strengthening its leadership, Alexandru Stefan Gheban, one of the company’s six co-founders and former CFO, has been appointed CEO, working alongside co-CEO Andrea Ferrero.

“Since 2018, each funding phase has progressively strengthened Young Platform’s operational capabilities and market presence, paving the way for ongoing innovation and expansion,” noted Andrea Ferrero. “With this new financial operation, we are pleased to receive renewed trust from an important partner like Azimut as we prepare to launch new products and services that will enable Young Platform to build the first Banking 3.0 platform. Our platform will be without borders, seamlessly blending elements of traditional finance (TradFi) with the innovative functionalities of decentralised finance (DeFi), helping to make global banking faster, cheaper, and simpler.”

Young Platform remains committed to adhering to regulatory standards, a company’s core value. The platform is registered with Italy’s OAM (Organismo Agenti e Mediatori Creditizi) and is authorised by France’s AMF (Autorité des Marchés Financiers). It also includes an in-house Anti-Money Laundering (AML) department. It aligns with the European Union’s new Market in Crypto-Asset (MiCA) regulations, which will be rolled out in the coming months.Azimut Holding CEO Giorgio Medda commented on the strategic significance of the investment: “Our investment in Young Platform aligns perfectly with our venture capital activities that aim to identify top-tier projects within emerging sectors.

Although cryptocurrency remains a complex field for many investors, it is essential to approach it with expertise, critical thinking, and a committed stance. Young Platform exemplifies these qualities, and we are confident that its team will continue to create innovative solutions that could positively impact the financial industry.”

Managing a personal budget is essential for anyone looking to save, invest, or simply gain control over their finances. If you’re wondering how to effectively handle your budget, we’ve compiled a list of the top budgeting apps that make money management effortless. These applications not only simplify tracking expenses but also help you avoid unnecessary spending—essential for those striving for financial security.

Forget about complex spreadsheets! With these apps, managing a budget is easy, enabling you to save more and plan for future investments. Here’s our top five picks for the best budgeting apps in the UK in 2024.

1. Spendee

Spendee is a highly effective budgeting app that stands out for its versatility. It enables users to link bank accounts, including some cryptocurrency wallets, making it easier than ever to track transactions and spending. This seamless connectivity means that users can stay updated on their finances in real time, eliminating the need for manual entry.

Spendee provides useful visual aids, such as graphs and dashboards, which offer insights into spending patterns. These tools make it simple to identify where most of your money goes, making it an ideal choice for anyone looking to reduce unnecessary expenses.

Key Features:

Bank account and cryptocurrency integration

Customisable charts and dashboards

Real-time transaction tracking

2. Copilot

Among the top budgeting apps, Copilot is unique due to its integration of artificial intelligence. This app acts as a digital personal finance assistant, offering spending insights and customised budget recommendations. While currently only available in the United States, Copilot has set a new standard for budget apps by providing tailored financial advice on the go.

As a finalist in Apple’s App Store Awards, Copilot’s cutting-edge features make it a standout option. With AI assistance, users gain personalised budgeting tips that help them stay on track with their financial goals.

Key Features:

AI-powered budget tracking and insights

Personalised financial advice

Winner of App Store Awards (US only)

3. YNAB (You Need A Budget)

YNAB is widely considered one of the best budgeting apps for those committed to financial discipline. The app’s core philosophy is to give every pound a purpose, encouraging users to allocate each penny towards specific goals. By dividing expenses into categories—such as savings, bills, or investments—YNAB enables a structured approach to budgeting.

For those who want a comprehensive tool, YNAB is ideal. It includes monthly planning features, educational resources, and workshops on financial literacy. YNAB aims not only to track expenses but also to improve your relationship with money.

Key Features:

Goal-oriented budgeting for each pound

In-depth tutorials and workshops

Monthly planning and detailed budgeting categories

4. Money Manager

For users who prefer simplicity, Money Manager is an excellent choice. It’s a straightforward budget app that allows for easy logging of daily income and expenses. The app categorises transactions automatically, giving users a clear overview of their spending patterns.

Money Manager provides helpful visual reports, making it easy to identify where you could cut back on spending. This lightweight app is perfect for anyone looking for a no-fuss way to manage their finances.

Key Features:

Simple transaction logging

Expense categorisation and visual reports

Lightweight design, ideal for users wanting a straightforward app

5. Wallet

The final app on our list is Wallet, another great choice among the best budgeting apps in the UK. Like Spendee, Wallet supports automatic bank account linking for real-time expense tracking. Wallet also allows for shared budgeting, which can be handy for families or couples managing joint expenses.

One unique feature of Wallet is its savings goals, where users can set financial milestones and track their progress. Push notifications provide reminders of your financial commitments, helping you stay focused and avoid impulse purchases.

Key Features:

Automatic bank account linking

Shared budgeting for group finances

Savings goals and notifications to keep you on track

Why Use Budgeting Apps?

Utilising one of the best budget apps can make financial management significantly easier. These tools can help you categorise expenses, identify overspending, and set financial goals—all essential for those aiming to boost savings and cut out unnecessary costs. Whether you are looking for a simple tracker or a comprehensive financial planner, there is an app that meets your needs.

With any of these apps, you’ll gain better visibility over your finances, helping you lay a foundation for more informed spending and saving decisions. When your budget is under control, you can consider exploring investments. A practical approach for beginners is recurring purchases, a strategy that allows you to invest incrementally and consistently.

By choosing the best budgeting app for your lifestyle, you can make financial management more straightforward and enjoyable. Start today with one of these budgeting apps and take the first step toward a secure financial future.

What is the state of the financial markets today? What are the principles to be observed when investing intelligently? Here is what emerged from J.P. Morgan’s latest report

What should an investor know today to be called ‘smart’? Last week, the S&P 500, the world’s largest stock market index of America’s 500 most capitalised companies, reached a new all-time high, its 46th of this year.

However, although major asset prices tend to be bullish in the long run, steering the markets is still a complicated business. Here are two principles an intelligent investor should know today.

The state of the market

First, however, it may be useful to analyse the state of the stock market. Results in 2024 were decidedly positive because most listed companies exceeded growth expectations. More than three-quarters of the companies exceeded expectations by 6.8% in aggregate. However, a few exceptions came from what many believe to be the most promising sector soon: artificial intelligence. For example, ASML, a leading Dutch semiconductor supply chain company, put pressure on chip stocks on Tuesday after missing earnings and revising its sales forecast 2025.

On the other hand, regarding the bond source, US government bond yields fluctuated throughout last week, then stabilised after releasing two important macroeconomic data: retail sales and unemployment benefit claims. Consequently, the current situation makes us cautiously optimistic about the FOMC meeting on 7 November 2024, after the committee still needs to meet in October. Will the FED and its chairman Jerome Powell cut interest rates again, as happened in September?

How can we not mention the US elections, scheduled for Tuesday, November 5? It is certainly important to follow what will happen, but it is not fundamental, as we will see by analysing two cardinal principles of the intelligent investor that we have extrapolated from the latest J.P. Morgan report.

Smart investing: the hygiene of your portfolio

The first crucial principle for J.P. Morgan to invest intelligently is portfolio hygiene. This term indicates the identification of clear objectives and the creation and maintenance of a long-term plan, all accompanied by regular ‘check-ups’. What does this mean from a practical point of view?

To understand this, we can extrapolate an example from the current market situation. Last week, we celebrated the second birthday of the current bull market, at least as far as the stock market is concerned. On 12 October 2022, the S&P 500 touched a low at 3,577 and has since recorded +60%. Although very positive for investors, this upward movement has certainly unbalanced the allocations of those who diversify between different types of assets, e.g., stocks and bonds. Therefore, if one’s strategy provides for it, it may be time to rebalance and stick to one’s plan.

For example, if we look at a 60/40 type portfolio (60% invested in stocks of the S&P 500 and 40% in US bonds), we see that it has had a total return of about 27% over the past year. Without rebalancing, the same portfolio would now be overweighted in stocks at 64% and underweighted in bonds at 36%, given the difference in return between the two asset classes. According to J.P. Morgan, a smart investor periodically takes the time to analyse their financial situation and make adjustments according to their strategy.

However, the preceding is not mandatory. If your strategy involves periodic investments, perhaps through recurring purchases, but does not involve periodic rebalancing, you can safely proceed without changing allocations. Consider extending your current approach to another innovative and promising market: cryptocurrencies.

Understand the risks, but prepare for the opportunities

The second principle of the ‘smart’ investor identified by J.P. Morgan ties in with what was specified at the end of the previous paragraph. In a market often influenced in the short term by macroeconomic and political news and events, it is important to look to the long-term and sound fundamentals.

Some topics that we have often discussed on our blog, such as the upcoming US presidential election, geopolitical turmoil in the Middle East and monetary policy decisions by central banks, may cause unease or arouse fear. However, they mustn’t affect one’s long-term strategy in any way. In the investment world and when trading in the markets, it is crucial to focus on knowledge, data, and tangible and concrete variables rather than unknowns.

In support of this thesis, J.P. Morgan presents some historical data, which shows that markets tend to rise regardless of the winner (or winner) of presidential elections. The same argument can also be applied to conflicts and central banks’ decisions on interest rates. Since 1950, there have been 18 elections in the US and ten changes in the White House between Democrats and Republicans. Over these 74 years, US GDP growth has averaged 3.2% per year, while that of the S&P 500 has averaged 9.4%. In short, an investor, if intelligent, should take the ball when he starts to doubt his investment strategy due to news or unexpected events and use the moment to re-examine his objectives,plan, and the time horizon of his investments.

In conclusion, according to J.P. Morgan, an intelligent investor does not change his strategy depending on the news or looming events. On the contrary, he constantly monitors the situation but only acts according to his plan and objectives.

Bitcoin has touched its all-time high. Will it break its all-time high in the coming days? Meanwhile, ETFs record performance

After several weeks of uncertainty and boredom, euphoria has finally returned to the crypto market, and suddenly, a newall-time high for Bitcoin is on the way. Its price rose above $73,000 yesterday, while it is now stable at $72,000.

The crypto market is now flooded with optimism, with many wondering whether this is the beginning of the most explosive phase of the 2024 bull market. Furthermore, Bitcoin’s breach of the ATH could trigger a further explosive move, as it could result in the liquidation (closure) of $2 billion of short positions.

Record-breaking Bitcon spot ETFs and retailers

Bitcoin’s recent pump may also have been caused by spot ETFs on Bitcoin, as they have attracted attention and a considerable amount of capital. Last week, there were $870 million in inflows in a single day, primarily driven by BlackRock’s iShares Bitcoin Trust, which continues to dominate the crypto ETF market.

In October alone, Bitcoin ETFs surpassed $3 billion in new investments, a sign of renewed institutional interest. BlackRock and Fidelity are among the main beneficiaries and architects of this boom, helping to bring BTC held by spot ETFs close to the historic one million mark.

However, while institutional interest drives the market, it is interesting to note that retailers (individual investors) still need to enter the market en masse, as shown by searches on the major search engines. However, Bitcoin’s approach to its ATH could catalyse a new wave of retail investors, who might be attracted by the FOMO that invades newspapers and social networks at these junctures. At least, this is what has happened during past cycles.

Bitcoin in pension funds: the Florida case

Another positive news from the crypto world is not concerned with the price of Bitcoin and its possible ATH; it is a more institutional topic: pension funds. Florida CFO Jimmy Patronis recently requested a feasibility report from the state’s board of trustees to invest part of pension funds in cryptocurrencies, focusing on Bitcoin. Patronis seems to be following the example of Republican candidate Donald Trump, who, during the ‘Bitcoin 2024’ conference in Nashville, proposed creating a national reserve with Bitcoins confiscated from criminals and failed companies.

Patronis’ proposal envisages the introduction of a pilot programme of investment in digital currencies within the Florida Growth Fund to test the possibility of integrating Bitcoin as a reserve to protect citizens’ savings from dollar devaluation and inflation. This vision is strikingly in contrast to the situation in Italy, where there is a discussion of increasing taxes on technology assets. While Italy considers higher taxation, Florida explores using Bitcoin as a potential tool to restore the pension system.

Finally, how about not mentioning the US elections, as the vote is less than a few days away and could add another element of volatility to the markets? Indeed, investor enthusiasm increases with Donald Trump’s chances of victory, which is considered more favourable towards the crypto sector. Some analysts suggest that his eventual pro-Bitcoin policy could consolidate BTC as a strategic reserve, fuelling an even stronger bull run.In short, the current scenario, characterised by the support of institutional investors and a possible influx of retailers, could allow Bitcoin to reach a new ATH soon. In any case, monitoring the market with rationality and scepticism remains crucial, remembering that euphoria can be just as dangerous as panic. Bitcoin’s explosive rallies are certainly exciting, but as always, caution is in order in the crypto world.

The Q3 2024 YNG Token Report – Key highlights and next steps

The latest quarterly report for the YNG token is here, bringing you a full update on recent developments and future milestones. What’s been happening in this action-packed quarter? And where are we heading next?

The YNG Token Report is essential reading for anyone following the progress of Young Platform’s utility token. It outlines the major steps we’re taking to introduce YNG to the decentralised market. This quarter’s strategy hinges on three core initiatives: buybacks, regular liquidityinjections, and both public and private sales. Full details on each can be found in the main report below.

What happened in Q3 2024?

Curious about what was achieved in Q3? The report details everything, including token issuance, purchases, sales, and the latest milestones achieved on the journey to decentralising YNG. In our roadmap to decentralisedmarketentry, you’ll also find updates on the broader token project and the current stage.

For a complete overview, read on to explore this October 2024 report.

Young Platform Club metrics: Q3 2024

YNG is the utility token of Young Platform, which provides members with access to exclusive subscription-based “Clubs” that reward our most committed supporters with unique benefits.

Currently, the Clubs include 1,659 members, split as follows:

Bronze Club: 1,172 members

Silver Club: 224 members

Gold Club: 131 members

Platinum Club: 132 members

Membership in these Clubs requires a locked balance of YNG tokens on the Young Platform exchange. This membership distribution demonstrates the token’s user base and influences market dynamics; the higher the Club membership, the lower the selling pressure on YNG, ultimately supporting price stability.

Since the launch of Staking, YNG holders have gained an additional benefit: token rewards provided through staking, exclusively in YNG. Full details on staking benefits can be found later in the report.

Membership Trends

Comparing these figures with those from Q2 2024 shows a slight decline in Club members, down from 1,699 to 1,659:

Bronze Club: 1,192 members

Silver Club: 230 members

Gold Club: 139 members

Platinum Club: 138 members

This represents a 3% decrease in membership numbers. However, recent updates to our ecosystem could shift this trend. In early October, we launched staking with enhanced rewards for Club members, and exclusive content from the crypto and finance event DYOR24 will soon be available to our most dedicated supporters.

YNG Token distribution and circulating supply

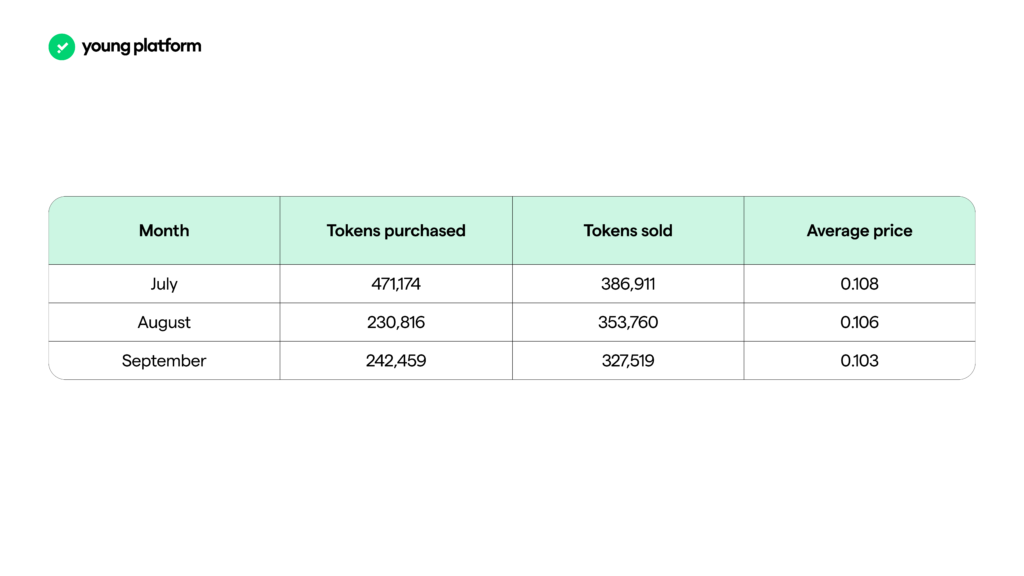

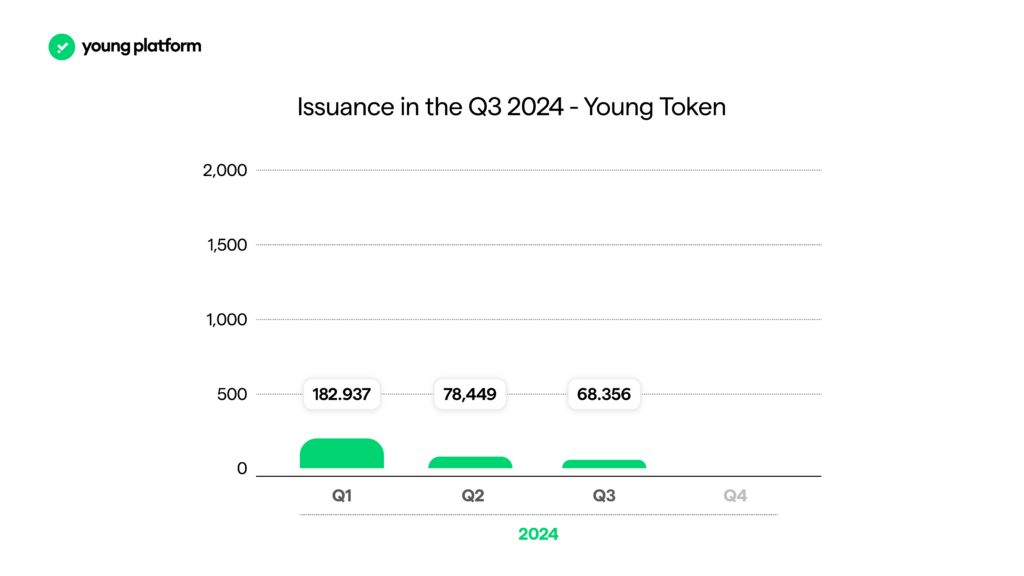

In June, the circulating supply of YNG was approximately 23.6 million, and by September, it had risen to around 23.67 million, marking a net increase of approximately 68,356 tokens, or 0.33%.

These tokens were allocated through various activities:

18,202 tokens were distributed via Quizzes, Challenges, and Up&Down (pre-Level implementation).

50,153 tokens awarded through Level completions.

YNG’s market operates through an algorithm managing the exchange rate using two underlying liquidity pools in EUR and YNG. At the May 2022 launch, these pools contained:

€1 million

4 million YNG

After accounting for buy and sell activities across Q3, by July 2024, the pools held:

€655,740

6.45 million YNG

This configuration reflects the token’s buy and sell dynamics over the past quarter, including price performance data presented later in the report.

YNG Token emissions in 2023

What happened in Q2 2024 in terms of Tokenomics?

The structure of YNG emissions saw its first major shift last year with the Step 3.0 updateand more recently, with the introduction of Staking. Regarding Step 3.0, we now have sufficient historical data to analyse its impact. For Staking, while still in the early stages, the initial results are aligned with our planned economic model, which we’ll explore further in this report.

As the chart illustrates, the latest Step update significantly curtailed YNG distribution, reducing new token emissions by 95%. A decrease in active users also influenced this outcome.

It’s important to highlight that YNG’s upcoming launch on the decentralised market will coincide with a full restructuring of its tokenomics. Specifically, our new features will channel token rewards exclusively to Club members, a model introduced with our latest Staking feature.

We anticipate a rise in YNG emissions starting in Q4 2024. However, increased Club membership and demand are likely to offset this, which could positively impact the token’s market dynamics.

YNG price analysis

YNG Price Trends in Q3 2024

Let’s examine YNG’s price movement throughout Q3 2024. Like Q2, the broader crypto market remained relatively stable over the summer, with Bitcoin trading within a narrow range of $67,000 to $55,000, showing no clear trend.

Similarly, YNG’s price exhibited low volatility, fluctuating slightly between $0.10 and $0.11.

Q3 2024 achievements

Our primary focus in Q3 2024 has been enhancing the Staking feature alongside ongoing developments in the YNG token project (which we’ll detail in a dedicated section). A key objective was to reintroduce the Earn feature, which we had paused in 2022, and to make significant strides toward regulatory compliance under the EU’s Markets in Crypto Assets (MiCA) framework, partially enacted in late June.

This report provides an excellent opportunity to summarise our recent work. Let’s review the initiatives undertaken in 2024 to increase the value of our Clubs and, in turn, boost YNG’s appeal.

Staking on Young Platform

A key focus of Q3 2024: Staking

The highlight of Q3 2024 has been the rollout of our Staking feature. Though there are many exciting changes compared to the Earn function active on Young Platform until the end of 2022, the main objective remains: allowing users to earn rewards on their crypto assets easily and simply. Whether you’re a seasoned investor or a newcomer to the crypto world, Staking offers a straightforward way to put your assets to work and maximise returns.

Staking on Young Platform brings two primary benefits:

Simplicity: Earn rewards without needing to navigate the complexities of decentralised protocols.

Accessibility: Start with as little as €50, making staking available to users with smaller portfolios.

A unique aspect we want to emphasise in this report is that Staking represents the first feature developed under YNG’s new economic model, which will be discussed in detail later. Beyond the standard rewards, our most loyal members receive additional YNG token bonuses.

We aim to engage and reward Club members by providing enhanced benefits within our ecosystem. The following YNG bonus rewards are available depending on the Club membership level. To calculate the total value of these boosts, simply add the percentage below to the standardstaking APY. The maximum additional percentage varies depending on the staked asset:

Bronze Club: up to +5%

Silver Club: up to +15%

Gold Club: up to +30%

Platinum Club: up to +70%

Check out our dedicated guides for a more in-depth look at how staking works and how to make the most of this feature!

DYOR24: a successful event

Last week, we hosted DYOR24, a free online event that brought together Italy’s leading crypto and finance expertsin one virtual space. It was a tremendous success! Our team’s efforts were validated by the fantastic feedback we received regarding the quality and accessibility of our speakers. At Young Platform, we’ve always aimed to foster an environment where people can explore, discover, and ask questions without hesitation, and DYOR24 embodied this mission in every session.

But there’s more! In the coming days, DYOR24 will become an exclusive benefit for Club members, who will gain access to recordings of every guest session. This first online event will transform into a professional course, with experts stepping into the role of “instructors” to deliver over 24 hours of in-depth lessons on a range of critical topics across crypto and finance.

New benefits for Club members

In recent months, we’ve introduced two additional perks for our Club members through exclusive vouchers:

Saily: In September, we launched Saily, an international eSIM service enabling seamless internet access worldwide. Developed by Nord Security, the creators of NordVPN (a brand we already partner with), Saily is perfect for staying connected no matter where you are.

Tiqets: We recently announced our partnership with Tiqets, a service that provides discounted and queue-free access to museums, attractions, and activities worldwide—from New York to Tokyo, Rome to Paris.

These new benefits, alongside our collaborations with WeRoad, Saily, and now Tiqets, offer Club members a fully enhanced travel experience. With WeRoad, members can explore the world through exciting group trips. Saily ensures they stay connected online, and Tiqets allows them to make the most of their travel experiences quickly and conveniently.

More partnerships on the horizon

The new benefits don’t stop here. We are talking with other prominent brands to continue providing our members with increasingly valuable and exclusive benefits. Stay tuned to our blog and social media channels to be the first to hear about what’s next!

Exciting developments ahead!

Here’s where things get really interesting. As hinted earlier, Q3 2024 saw us focus on Staking and early groundwork for our upcoming Payment Account feature. Meanwhile, the YNG token has remained at the core of our efforts, with significant progress and a clear roadmap for its future—a main focus of this report.

Payment account & Card

As mentioned in the previous report and our dedicated AMA, we’ve been working on something special, a long-term project we’re thrilled to bring back into focus thanks to new opportunities that allow us to expand our vision.

This upcoming feature merges the best of traditional and digital finance into one seamless experience, elevating your daily interactions to something truly revolutionary. Rather than simply providing a tool, we aim to introduce a feature that integrates fully with our ecosystem, setting us apart from competitors. Our goal is to launch the Payment Account and its accompanying Card by the end of Q1 2025, and we are positioning the Clubs and YNG token to play a central role in this ecosystem.

New Staking developments

The Staking feature, launched on 7 October, is just the beginning. In addition to app integration and the ability to stake Solana (SOL), we’re actively working to expand staking options across a broader range of cryptocurrencies, enabling users to earn rewards on more assets they hold.

As always, we welcome user feedback to guide us in implementing new staking options that best meet our community’s needs.

Tokenomics: the evolution of Young (YNG)’s Economic Model

In Q3, we reviewed and refined the documents created in Q2, incorporating valuable feedback from fund managers and advisors. Alongside these refinements, we developed an enhanced economic model for YNG, positioning it as a core driver of engagement within our ecosystem and directly rewarding user participation.

A live session initially planned for our Platinum Channel members was postponed over the summer due to essential revisions, but it will now be rescheduled following the AMA for this report to cover all the latest updates.

With the recent launch of staking, many of you have noticed that YNG has evolved beyond its previous role as a simple reward in Step. YNG will be integrated across most of our platform’s features, incentivising activities like learning, trading, and transactions and making Club membership more appealing.

New YNG Model: incentives for platform engagement and Club Membership

Our revised YNG model is designed to reward user activity and promote Club membership. Every interaction on the platform—whether educational, trading, buying, or selling—earns users rewards, thus enhancing the value of joining our Clubs. This approach draws in new users and encourages our existing community to participate more deeply, fostering organic growth, a balanced token economy, and long-term sustainability.

Key features of the new model and the upcoming steps towards decentralised market entry include:

Reward Structure

Our reward system aims to attract new users and boost community engagement. By offering a variety of incentives linked to user actions, we are promoting Club participation and building a more vibrant, dynamic community. Here’s an overview of our primary reward structures:

Learn Reward: Users earn YNG by engaging with educational content and games on the platform. This initiative rewards learning and commitment, helping users expand their financial knowledge while strengthening their connection to our ecosystem.

Staking Reward: Club members who use our staking feature (or staking services from third parties like LIDO, available through the platform) receive additional YNG rewards. This mechanism encourages Club participation and engagement with our ecosystem’s features without substantially increasing token circulation.

Card Cashback: Transactions made through the upcoming “Payment Account & Card” feature will earn users cashback in YNG. This reward structure is designed to maximise the benefits of everyday transactions and encourage the use of the payment account.

Exchange Cashback: Users will also receive cashback in YNG on trading fees, which is designed to boost trading activity and increase platform interaction.

Each of these reward structures is designed to make YNG a central and valuable asset within our ecosystem. They fairly reward users while encouraging them to explore and use the platform’s full suite of features.

YNG Treasury

The YNG Treasury is a fundamental pillar of the token’s economic model, designed to ensure stability and support long-term growth. It will accumulate some fees generated from YNG reward-based platform activities and funds raised in upcoming sales stages. These funds will be strategically allocated to activate the stabilisation mechanisms described below, ensuring sufficient liquidity to maintain balance in the token market.

Additionally, the treasury will serve as a reserve to fund YNGdevelopment, marketing, and promotionalinitiatives, supporting the expansion of the ecosystem. Prudent management of treasury funds will sustain a long-term, balanced model, encouraging organic community growth and reinforcing YNG as a valuable asset for users. We are committed to maximum transparency in treasury fund use, providing periodic updates to allow the community to monitor and assess treasury operations.

Stability mechanisms

The economic model for YNG includes various mechanisms designed to stabilise and sustain the token in the long term. Our strategy seeks to balance YNG demand and supply dynamically, ensuring price stability and fostering communityengagement. Here are the primary tools to achieve this balance:

1. Club entry token rebalancing: This will be the first mechanism activated, with a start date announced after consulting Club members. The mechanism periodically adjusts the number of YNG tokens required for Club access based on price fluctuations. If YNG’s price rises compared to the previous period, the token requirement will decrease by 50% of the price increase. Conversely, if the price decreases, more tokens will be required without an additional 50% on the rise.

Example: If YNG’s price rises by 10%, the token requirement drops by 5%. If the price falls by 10%, the token requirement increases by 10%. This adjustment will start from the current entry requirements, based on the original listing price of €0.24, balancing accessibility with user commitment while rewarding early adopters who join Clubs before new features arrive.

2. Add Liquidity: The Add Liquidity function ensures two conditions are met before adding EUR and YNG tokens to the liquidity pool:

Monthly Budget: Ensures sufficient monthly treasury or revenue funds are allocated to liquidity.

YNG Availability in Treasury: Confirms the treasury holds enough YNG for liquidity addition.

When both conditions are satisfied, liquidity is added to the pool, helping to stabilise or boost liquidity and mitigate significant price fluctuations for YNG.

3. Buyback: The Buyback function is also regulated by the monthly budget, allowing the platform to purchase YNG from the market using treasury EUR. This reduces YNG’s circulating supply and supports its price. A buyback occurs only when adequate funds in the treasury cover the transaction amount, ensuring controlled management of YNG supply and price stability over time.

The coordinated implementation of these mechanisms is designed to ensure stable YNG liquidity, promote organic community growth, and support the ecosystem’s evolution. Our model is built around Club membership growth, retention rates, and market dynamics, which we will continuously monitor. Adjustments to rewards and stabilisation mechanisms will be made to maintain economic stability.

Roadmap to the Decentralised Market

Before delving into our roadmap, let’s take a moment to reflect on what we’ve achieved since Young Platform’s founding in 2018. Over the years, we’ve built a robust ecosystem for YNG, navigating regulatory challenges, earning our community’s trust, and setting the stage for a sustainable decentralised market. Each phase has been part of a well-defined strategy designed to stabilise the token, drive platform growth, and deliver real value to our users.

Phase 1: YNG Airdrop

Completed in June 2022, this phase marked the beginning of Young Platform products and the buy-sell availability of YNG at a fixed price of €0.24. The goal was establishing a stable foundation for YNG, adhering to regulatory requirements and building a solid platform for subsequent developments.

Phase 2: Community Market Pair

Currently underway, this phase introduced a proprietary Automated Market Maker (AMM), enabling the community to participate directly in a controlled and stable market environment. This phase has absorbed initial token sales and monitored user behaviour, creating a foundation for sustainable market management.

Phase 3: Engage to earn and decentralised transition

Scheduled for early 2025, Phase 3 will bring YNG into the decentralised market. This transition will coincide with the launch of our new reward structure, designed to incentivise user engagement and deepen community interaction.

Preparations for Decentralised Launch

To support Phase 3, we’ve outlined a series of preparatory steps to guide YNG into the decentralised market between Q4 2024 and Q1 2025:

Pre-TGE Buyback: This phase involves purchasing YNG tokens “on the market” to rebalance existing liquidity pools. The aim is to establish a strong price foundation for YNG before the official decentralised market launch. To simplify communication, we’re referring to the end of this launch campaign as the TGE (Token Generation Event) within our operational plan.

Private Sale: Select YNG tokens will be offered to venture capitalists, attracting strategic investors to support the project’s growth. Funds will bolster the treasury, finance development initiatives, and support buyback programmes. Private Sale participants will receive tokens on a structured vesting schedule over four years.

Suspension of YNG Trading on Young Platform and IDO Preparation: Before the IDO, YNG on Young Platform trading will be temporarily paused to facilitate a smooth transition to the decentralised market. During this stage, the IDO reference price will also be established.

IDO Sale: A portion of YNG tokens will be distributed through an IDO platform to increase the project’s visibility in the retail decentralised market. Funds raised will support liquidity management, contributing to token stability.

TGE and Decentralised Market Launch: This final stage will involve creating liquidity pools for YNG using decentralised protocols. Existing centralised pools will be migrated, and liquidity will be enhanced with funds raised in prior stages to ensure a strong foundation at launch. This step will consolidate YNG’s presence in the market, encouraging sustainable growth and greater accessibility.

That’s all for now—stay tuned on our channels!

The services offered, and the YNG token are and will remain available in compliance with applicable regulations, particularly the Markets in Crypto-Assets (MiCA) framework. We are committed to ensuring that every aspect of the project aligns with regulatory requirements, fostering a transparent and responsible approach towards our community and investors. Additionally, the company reserves the right to modify the services and YNG token features outlined in this document in response to regulatory developments and/or market conditions. Any updates will be communicated promptly to keep all users informed.

Earn new tokens with Ethereum, Cosmos, Celestia and Solana Staking.

Young Platform brings back one of its users’ favourite features: staking. With a wholly renewed approach designed to meet everyone’s needs, staking is once again one of the simplest and most effective ways to earnnewcryptocurrencies effortlessly. Whether you are a seasoned investor or a beginner just stepping into crypto, this is your chance to put your assets to work and maximise your returns.

Discover all the new staking features on Young Platform, and get ready to see your assets work for you!

Staking on Young Platform is straightforward. You can stake your cryptocurrencies to earn rewards without the complexities of decentralised protocols. The platform guides you step by step, and you don’t need significant capital to start: with a minimum of around €50, you can activate your stake and generate rewards.

Staking on Ethereum

Young Platform offers liquid staking for Ethereum (ETH)through the provider Lido. This approach allows you to earn new coins as rewards from the day after activation. Rewards are calculated as APY (annual percentage yield) and are credited daily, helping you see your balance grow day by day.

Staking on Solana

Young Platform offers an additional opportunity to use your cryptocurrencies with Proof of Stake for Solana (SOL). With this method, your SOL will support the blockchain network, and you’ll receive rewards every three days for your contribution.

Staking on Celestia and Cosmos

Young Platform provides another opportunity to make your cryptocurrencies work for you with Proof of Stake for Cosmos (ATOM) and Celestia (TIA), through a partnership with the provider Kiln.

Recurring Staking

Recurring staking, combined with recurring purchases, is a smart strategy for those with a long-term approach. While staking allows you to earn rewards passively by locking your assets, recurring purchases let you gradually accumulate cryptocurrencies, reducing the impact of volatility through Dollar Cost Averaging. Together, these two options create a synergistic effect: you increase your holdings over time and maximize returns with staking rewards, all without constantly monitoring the market. This approach combines financial discipline with long-term growth, making it ideal for building a robust and rewarding portfolio.

Exclusive benefits for Young Platform club members

For Young Platform Club members, staking becomes even more rewarding. In addition to the standard rewards in ETH or SOL, Club members also receive a bonus in Young (YNG) tokens. This means that for every stake activated, you receive not only the usual rewards but also an additional quantity of tokens, helping you maximise the value of your portfolio.

Don’t wait: the new staking on Young Platform is here, ready to help you grow your crypto easily and profitably.

Young Platform reopens its Staking functionality: here are all the updates

Young Platform is bringing back one of its most beloved features: staking. Completely revamped with new characteristics and advantages, staking remains one of the easiest ways to make your cryptocurrency holdings grow. Let’s explore the updates together!

Imagine you have a stash of cryptocurrencies. Generally, the value of these holdings doesn’t grow unless you delve into complex trading strategies, which require constant monitoring and can be quite stressful.

In other words, beyond just waiting for market prices to rise, it’s strategic to increase the number of tokens you hold. You could do this through trading or savings schemes, but there’s also a simpler way: staking. Staking allows you to increase the number of tokens in your wallet without selling your assets. This isn’t magic; it’s an inherent feature of how some blockchains work.

Staking exploded in popularity in 2020, particularly in decentralised finance (DeFi), because it offers a relatively simple way to earn cryptocurrency rewards.

Staking is linked to Proof of Stake (PoS) consensus protocols. Forget the powerful miners, costly hardware, and hefty electricity bills to “mine” new coins. With staking, you only need to “lock” your cryptocurrencies within a network and start receiving rewards.

How does Staking work?

Staking transforms the mere possession of cryptocurrencies into something more active and participatory. It’s a way to contribute to the security and efficiency of a blockchain network—and in return, you get rewarded.

Blockchain networks that use the proof-of-stake (PoS) consensus mechanism select validators from those who have staked their cryptocurrencies. These validators are responsible for verifying and confirming transactions and creating new blocks in the blockchain.

In exchange for their contribution, the network rewards these validators with newly minted coins as an incentive to participate and behave honestly. The system generates these coins as part of its protocol, similar to how miners earn cryptocurrency rewards in proof-of-work (PoW) blockchains. This process keeps the network decentralised and secure and distributes new tokens, encouraging active participation.

Staking protocols aren’t always user-friendly. Most DeFi platforms require technical knowledge, and navigating the maze of decentralised protocols can be challenging for those unfamiliar with the sector. Some centralised exchanges, like Young Platform, have developed solutions that make staking simple and accessible.

Lower budget requirements

The high minimum deposit requirement is one of the biggest obstacles to direct staking. For example, with Ethereum, one of the leading cryptocurrencies, staking directly on the Ethereum network requires a minimum of 32 ETH. With the current price of ETH around €2,000, that’s an initial deposit of approximately €64,000—not exactly pocket change.

This is where centralised and decentralised platforms come in. With services like those offered by Young Platform, you can start staking with a minimum of about €50 at current rates, making staking accessible for those with significant capital and those looking to start with a more modest amount.

Flexibility

You can cancel your staking at any time, provided that the platform allows it, giving you the freedom to manage your cryptocurrencies as you see fit.

Staking on Young Platform

Young Platform offers two types of staking: Liquid Staking and Proof of Stake, which can be used simultaneously. This allows you to diversify your portfolio and maximise reward opportunities across multiple blockchain networks.

Rewards are calculated through the APY (Annual Percentage Yield), which represents the net annual return. The APY shows the percentage of new tokens you can accumulate over 12 months, which is gross of the applied fees.

You can also create multiple stakes on available cryptocurrencies. You can create a new stake whenever you purchase or deposit new cryptocurrencies. In the “Stake History” section of the platform, you can track all the details: rewards generated, time elapsed since each stake was activated, and their value in euros.

When you create a new stake, you can see potential rewards and their equivalentvalue at the current price. This tool allows you to perform simulations and estimates, helping you plan your actions to meet your long-term goals.

Liquid Staking – Ethereum (ETH)

Liquid Staking allows you to stake your tokens while maintaining liquidity, making it ideal for those seeking greater agility. On Young Platform, this option is available for Ethereum (ETH)through the provider Lido.

With Lido, staking is managed directly on behalf of the user. Lido handles the staking, manages nodes, and distributes rewards. This process adheres to network activation and deactivation queues, ensuring that users can participate without having to directly manage nodes.

Asset: Ethereum (ETH)

Provider: Lido

APY: Lido provides the APY, which is calculated as an average over the last 30 days. The displayed APY is the gross of the applied fees.

Reward Currency: ETH

Compound Interest: Rewards are automatically reinvested into staking, increasing your total balance over time.

Minimum Amount: 0.02 ETH (use the Ethereum Converter to calculate the current value)

First Reward Credit: Approximately 1 day. This timing may vary depending on network conditions.

Reward Credit Frequency: Rewards are credited daily.

Thanks to Liquid Staking with Lido, you don’t need to worry about the complexities of node management. Lido takes care of everything, from managing nodes to distributing rewards, allowing you to participate in Ethereum staking without technical barriers. Moreover, you benefit from compound interest, which grows your balance over time.

Compound interest in staking works like a snowball effect: the longer you keep your cryptocurrencies staked, the greater the potential rewards accumulated. This approach rewards patience and consistency, making staking not only a strategy for immediate rewards but also a method to steadily increaseyour portfolio’s value over time.

However, it’s important to remember that past returns do not guarantee future results, and the value of cryptocurrencies and staking rewards can fluctuate.

Proof of Stake – Solana (SOL)

Proof of Stake (PoS) on Young Platform will soon be available for Solana (SOL) through the provider Fireblocks. This model selects validators based on the amount of tokens locked in the network. The more tokens you lock, the higher your chances of being selected as a validator and earning rewards.

Asset: Solana (SOL)

Provider: Fireblocks

APY: The APY is the rate the network recognises for validators at that moment. The displayed APY is the gross of the applied fees.

Reward Currency: SOL

Compound Interest: Rewards are automatically reinvested into staking, increasing your total balance over time.

Minimum Amount: 0.3 SOL (use the Solana Converter to calculate the current value)

First Reward Credit: Approximately 4 days

Reward Credit Frequency: Rewards are credited every 2-3 days, depending on network conditions.

The network distributes the rewards for Solana at the end of each “epoch.” An epoch lasts, on average, about 2.5 days, which is 60 hours. However, this period is not fixed and can vary depending on the state of the blockchain. For example, if the network is congested, the duration of an epoch may be longer. In any case, the minimum duration is 60 hours.

It is important to note that you must wait for two epochs to receive the first reward after staking SOL. This means it takes at least 96 hours (4 days) to receive the first reward.

Solana’s Proof of Stake is ideal for those who prefer a more traditional staking option. Unlike liquid staking, rewards here do not take advantage of compound interest, but you can still accumulate new SOL by actively participating in the network.

Proof of Stake – Cosmos (ATOM)

Thanks to the collaboration with the provider Kiln, the Proof of Stake (PoS) on Young Platform is available for Cosmos (ATOM). This system allows you to actively contribute to the security of the blockchain network by staking your ATOM and automatically earning periodic rewards.

Asset: Cosmos (ATOM)

Provider: Kiln

APY: Approximately 18%. The annual percentage yield (APY) corresponds to the rate at which the network grants validators at that specific moment. The APY is also gross of the applicable fees.

Reward currency: ATOM

Compound interest: Rewards are automatically reinvested into staking, increasing your total balance over time.

Minimum amount: 10 ATOM

First reward credit: 1 day

Reward frequency: 1 day

Proof of Stake – Celestia (TIA)

Young Platform also offers Proof of Stake (PoS) for Celestia (TIA) in collaboration with the provider Kiln. With this system, you can put your TIA to work to support the blockchain network and earn rewards simply and automatically.

Asset: Celestia (TIA)

Provider: Kiln

APY: Approximately 9%

Reward currency: TIA

Compound interest: Rewards are automatically reinvested into staking, increasing your total balance over time.

Minimum amount: 10 TIA

First reward credit: 1 day

Reward frequency: 1 day

Extra benefits for Young Platform Club members

For members of a Young Platform Club, an exciting new feature makes staking even more advantageous. Alongside receiving rewards in the cryptocurrency you’ve staked, like Ethereum (ETH), you’re also entitled to an additional APY in YNG tokens. This means you will receive the cryptocurrency you staked and a second reward in YNG tokens for every stake activated.

This dual benefit furthers the value of your portfolio, ensuring greater diversification and potentially better results over time. Club members can thus maximise staking returns, taking advantage of rewards in two different assets with each operation.

Ready to Take Action?

Check out the guide for activating staking on Young Platform and start putting your crypto to work today!

Staking, like any operation involving cryptocurrencies, comes with risks. The value of cryptocurrencies can fluctuate, and staking rewards are not guaranteed. Past returns do not indicate future outcomes and staking rewards can vary depending on factors such as the specific cryptocurrency protocol, the number of validators, and market conditions. It’s crucial to conduct thorough research and fully understand staking mechanisms before proceeding. Young Platform is committed to providing clear and transparent information but cannot be held responsible for any losses or damages resulting from the use of staking services. Users acknowledge that potential risks and/or attacks on one or more blockchain

Learn how to activate on-chain staking and earn new cryptocurrencies as rewards automatically and regularly.

What is Staking?

Staking allows cryptocurrency holders to participateactively in a blockchain network by “locking up” a portion of their assets for a certain period in exchange for rewards. Simply put, by staking, you’re contributing your crypto to support the network’s functionality and security, and you earn new crypto in return.

In staking, the right to validate transactions is linked to the number of coins “locked” in a wallet. Like mining in Proof of Work (PoW), stakes are rewarded for verifying transactions or finding new blocks. This reward is paid in the form of new tokens.

Note: Staked assets cannot be traded or used for buy/sell orders during the staking period, as they are locked on the blockchain.

Why does staking offer rewards?

Staking rewards come from the consensus mechanism of specific blockchains, such as Proof of Stake (PoS). By staking, you help validate transactions and maintain the network’s security, ensuring its decentralised and secure operation. In return, you earn new tokens, depending on how much you stake and how long it’s locked.

Note:

The more tokens you stake, the greater the rewards.

The longer you stake, the higher the rewards.

Staking on Young Platform

Young Platform offers two types of staking:

Liquid Staking on Ethereum (ETH)

Proof of Stake on Solana (SOL), Cosmos (ATOM) e Celestia (TIA)

Ease of Use: Young Platform’s centralized platform provides a simple staking experience, making DeFi accessible even to those unfamiliar with the space.

Convenience: Easily stake your idle assets and receive new tokens proportional to the staked amount.

Regular Payments: Earn rewards according to the blockchain protocol.

Flexibility: Closing your stake at any time after activation.

Security: Young Platform uses industry-leading providers to ensure safety.

Minimum and Maximum Staking Amounts

Ethereum (ETH): Minimum 0.02 ETH; Maximum 3 ETH per single stake.

Solana (SOL): Minimum 0.3 SOL; Maximum 75 SOL per single stake.

Cosmos (ATOM): Minimum 10 ATOM; Maximum 1000 ATOM per single stake.

Celestia (TIA) Minimum 10 TIA; Maximum 1000 TIA per single stake.

Total Maximum Amounts

Ethereum (ETH). Total quantity maximum in stake 300 ETH

Solana (SOL). Total quantity maximum in stake 4500 SOL

Cosmos (ATOM).Total quantity maximum in stake: 10.000 ATOM

Celestia (TIA). Total quantity maximum in stake: 10.000 TIA

For larger amounts, you can create multiple stakes of the same cryptocurrency.

Use the converters below to see the equivalent value in Euros:

You need a minimum amount of crypto to activate staking. Here’s how:

Deposit funds to your account via bank transfer or card (read the guide).

From the homepage, click “Buy”.

Select Ethereum or Solana.

Enter the amount.

Click “Continue” to complete the purchase.

Note: You can stake a single coin or multiple coins simultaneously.

Step 2: Choose Staking

Access the “Staking” section from the homepage. Alternatively, enter the dedicated section for these cryptocurrencies from the SOL, COSMOS, TIA or ETH Market Page or your wallet.

Select the type of staking: Proof of Stake or Liquid Staking. If the cryptocurrency supports both types, you can activate both.

Understand the APY (Annual Percentage Yield): You’ll see an APY figure representing the potential yearly yield during the selection. It’s an average of the last 30 days (for Ethereum) or that recognised by the network at that precise moment (for Solana, Cosmos, Celestia) and may vary depending on market conditions. Therefore, this value may vary over time. The APY is shown after the applicable fees.

Note: Rewards are credited to the staked cryptocurrency. E.g., if you stake ETH, you earn new ETH tokens.

Step 3: Activate Staking

After selecting the type of staking, you’ll see its details, including:

Club Reward: Members of our Club receive extra rewards in YNG tokens.

Activation Time: The time required for staking to go live on-chain after creation. During this period, no rewards are earned.

Reward Credit: Frequency of rewards and whether they’re compounded automatically.

Closing Time: The time needed to unlock your assets and transfer them back to your main wallet upon stake closure.

Note: Each protocol has a different structure and staking mechanism. These protocols are maintained and supported by various third-party projects that are distinct and separate from Young Platform

Step 4: Insert Amount

Read the information sheet and enter the amount of crypto you want to stake. Remember to check the minimum required for each coin. Thanks to the euro equivalent displayed, you’ll know exactly how much you’re staking in traditional currency.

Once confirmed, review the summary and finalise.

Note: The euro value of the rewards is calculated by applying the APY to the staked amount. However, this is only an estimate—actual rewards may vary due to market conditions and the network status.

Monitoring your staked assets

Once activated, monitor your stakes in the Active Staking section. You can also view the stake’s history, current status, and any earned rewards. Possible states include:

ACTIVATION: Staking is being activated on the blockchain.

ACTIVE: Staking is live, and you’re earning rewards.

CLOSING: You’ve requested to close the stake; the assets are unlocking.

CLOSED: Staking is fully closed, and rewards are no longer earned.

In this summary screen, you’ll also see:

Staking Reward: the total new crypto you have received as a reward.

Club Reward: YNG tokens earned.

History: Includes creation date, activation date, first reward date, and more.

Rewards begin accruing only after the validator activates and processes staking. If you withdraw early, rewards may not be paid. Rewards are based on estimated validator earnings, which are the gross of the Young Platform’s fees.

Young Platform does not guarantee specific rates or returns. The first reward might take longer due to activation time and validator performance.